Trust Awards 2014: UK Equity Income

9th July 2014 16:42

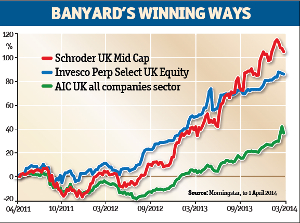

Winner: Schroder UK Mid Cap Fund

Investors appear to have an abiding enthusiasm for the UK equity income sector, but in terms of total returns, most of the better three-year performers in the UK mainstream sectors have been relatively low yielding.

is a case in point. It has a well-covered dividend, which has grown by a very useful 7.8% over the past five years, but its yield is only 1.6%.

It wins this award with the best three-year net asset value (NAV) returns in the sector bar , which misses out because it did not make the cut for our awards in 2011/12. Over the three years to March 2014, both trusts handsomely outperformed the FTSE 250 index, which in turn handsomely outperformed the FTSE All-Share index.

She had warned for some time that it was becoming difficult to find attractively priced new ideas. She sold a number of holdings last year because they looked fully valued and "took the top off" others in February and March for the same reason. All the trust's gearing was paid off in early April.

Banyard points out that one of the main reasons for the recent setback has been earnings downgrades due to the strength of sterling; around half the revenue of portfolio holdings comes from overseas.

Problems in the Ukraine and Russia have also affected some companies, while the battle for encouraged non-specialist UK equity managers to move money out of mid-cap shares and back into mega caps.

She fears sterling strength could continue to damage company earnings for some time. She is steering clear of the latest batch of initial public offerings, as she thinks they are generally overpriced.

On a technical valuation issue, she is worried that some companies appear to be boosting their earnings by using IFRS accounting methods that allow some costs to be put on a balance sheet and called assets, and others put below the line (i.e. non-recurring) and called exceptional items. This led her to sell and .

| Managed by Rosemary Banyard since 2003 | ||

| Sector | UK all companies | |

| Three-year NAV total return | 76.1% | |

| Three-year share price total return | 104.3% | |

| Discount | -2.6% | |

| 12-month range | -14% to 0% | |

| Average for sector | -7.6% | |

| Ongoing charges | 1.58%* | |

| Notes: Figures to 1 April 2014. *Includes performance fee. | ||

| Website: schroders.co.uk | ||

However, she is anxious not to sound too gloomy and is pleased that the correction in the FTSE 250 index has left better value on offer. "Things that got smacked were mostly highly rated - I have been able to top-up my holding in below 1,000p a share, having taken some of my profits earlier in the year above 1,600."

Highly commended: Invesco Perpetual Select UK Equity Trust

The smallest of the UK equity trusts managed by Mark Barnett, has a very similar portfolio to and , but has marginally outperformed both in each of the past three years.

It has a more concentrated portfolio, with 50 holdings compared to 60-plus with PI&G, and a higher weighting in large and very large companies, headed by , and . It does, however, have some exposure to mid-cap shares and did well last year from the recovery at and . Gearing has averaged around 10%.

In what he terms "a low growth world", Barnett has consistently focused on companies which have regularly grown their revenues, profits and free cash flow, and whose managers "are fully cognisant of the need to deliver sustainable, long-term dividend growth".

Recently promoted to head of UK equities at Invesco Perpetual, Barnett has been a long-term backer of tobacco stocks and of "big pharma", including , Roche and AstraZeneca. He was not keen on recent bid.

He believes positive sentiment towards equities has been driven by loose monetary policy and expects the market to be volatile as it is withdrawn. However, he is confident his own portfolios still offer good value.

Shares in IP Select UK Equity Trust are convertible at quarterly intervals into the other share classes of IP Select. As a result virtually all the trust's income is paid out each year. The dividend yield, at 3.6%, is therefore relatively unpredictable, as it is on open-ended funds.

Editor's Picks