Share Sleuth's July Watchlist

15th July 2014 09:26

Each month Richard Beddard trawls through annual corporate results for his Watchlist and the Share Sleuth portfolio of companies that satisfy key valuation metrics such as earnings yield and return on capital - and profiles the most interesting candidates.

This month the spotlight is on the growing Anpario, an animal feed additive producer, as it looks to expand into huge markets such as Brazil, China and the US. This will be risky, though, as antibiotics, which are much cheaper than natural additives, are still in widespread use.

One company not joining the watchlist, though, is business process outsourcing company Xchanging. Ther firm, whose most profitable niche is insurance, has joined the "too difficult" pile due to its complex accounting practices and a changing business model.

Watch: Anpario

Were it not for the cost of investing in subsidiaries in Brazil, Malaysia and the US, the company's performance might have been better. It's targeting the world's biggest poultry and pig producing countries: China, Brazil and the US, which account for more than 50% of global production.

The banning of antibiotics to promote animal growth is forcing producers to consider alternatives such as Anpario's Orego-Stim, an essential oil supplement that increases animal size, fertility, health and palatability. The company says its natural additive formulations are trademarked, complex and resistant to reverse engineering.

It's still early days for the company's growth strategy. Anpario registered its products in China in 2010, and in 2013 China brought in about 10% of total gross profit. However, local subsidiaries will enable Anpario to register products in its own name and market directly to customers.

Entering new markets is risky. Antibiotics, which are much cheaper than natural additives, are still in widespread use, even in Europe, where they have been banned since 2006. Synthetic additives and rival natural additives also offer competition.

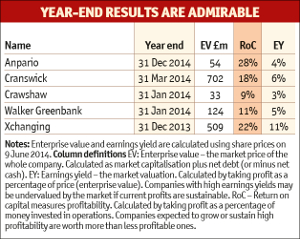

Nevertheless, Anpario is developing its most profitable products and selling them in the biggest markets. The company's promise is probably reflected in its share price of 285p. That values it at about £50 million, about 23 times adjusted 2013 earnings. The earnings yield is just 4%.

Watch: Cranswick

Revenues at rose 14% for the year to March 2014. Adjusted profit increased by 6%, and the company's overall level of debt fell a little. Cranswick produces meat-based foods such as sausage, principally for premium supermarket brands, including the Sainsbury's Taste the Difference and Tesco Finest ranges. It also supplies manufacturers and the food service industry.

Cranswick has been moving up the value chain from animal feed cooperative to farmer, to meat producer concentrating on premium products, to manufacturer of things with meat in them. In the year to March 2014 it acquired two pig farms, giving it more control over supply at a time when traceability and food safety are a major concern for supermarkets.

The biggest risk facing Cranswick may be that three customers, all supermarkets, accounted for 61% of its sales in 2014. Size gives supermarkets fearsome bargaining power, and Cranswick could, as it did in the year to March 2014, find itself caught between downward pressure on the price of food it has produced and increases in the cost of raw materials such as pork.

Cranswick's record of revenue, profit and dividend growth should give investors comfort, though, as should current profitability. Over the full year, return on capital was 18%. The company achieved these returns by focusing on premium products, which customers do not expect to buy cheaply, and building close relationships with customers and suppliers.

Perhaps Cranswick, like its sausages, is worth a premium price. A share price approaching £1,290p values the enterprise at £700 million, equivalent to about 17 times adjusted 2014 earnings. The earnings yield is 6%.

Watch: Crawshaw

In the year ending 31 January 2013, achieved a sharp improvement in adjusted profit - up 71% on the previous year, with a 12% increase in revenue and an 11% decrease in overall debt. The company had minimal bank borrowings.

Growth may be the product of a unique strategy that a combination of recession and experimentation has masked since Crawshaw floated in 2008. It has struggled to achieve adequate profitability, but in 2014 it managed a respectable 9% return on capital.

Crawshaw sells good-quality meat cheaply. It competes with supermarkets and butchers' shops, but it sources, processes and sells meat itself. It has a core product range, but it also buys surplus meat cheaply on the 'spot market', packs it up in value packs and sells it at key price points - £5 is popular. To shift meat quickly, staff call out the bargains market-trader style. It claims to be able to beat supermarket prices by up to 40%.

The company operates 21 stores, up from 14 in 2008, and two processing and distribution centres in Rotherham and Grimsby. It plans to open at least two more stores a year and it is developing online shopping.

The promise of this innovative business in an unfashionable sector is dimmed somewhat by the fact that its shares are popular. They have increased in price more than tenfold from penny stock levels in 2012. A share price of 40p values the firm at just under £30 million, 30 times adjusted 2014 earnings. The earnings yield is 3%.

Watch: Walker Greenbank

Wallpaper manufacturer revealed continued growth in the year to January 2014. Revenue was up 4% and adjusted profit up 13%. The company earned a healthy return on capital.

Walker Greenbank designs and manufactures furnishing fabrics and wallpapers. Harlequin and Sanderson, the two biggest brands by revenue, grew in 2013.

The company's UK market leadership stems from design, which Walker Greenbank says enables innovation when coupled with its manufacturing capability. It operates three studios and two UK factories. In 2013 it invested in a £1.75 million rotary/gravure machine, which allows it to combine two printing techniques to produce a new, premium textured wallpaper, Anthology.

It plans to grow internationally and by licensing designs. Licensing, principally to manufacturers of bed linen and rugs, brought in £2.1 million in 2013. That is just 3% of revenue, but it makes a big contribution to profit because it is effectively a royalty payment. The company earns 23% of revenue abroad. It has opened a new showroom in Dubai and is extending and redesigning its New York showroom. It already has showrooms in Paris, Moscow and Shenzhen.

Established brands may give Walker Greenbank a competitive advantage, which it is seeking to exploit by developing products for more customers. It invests heavily, so it remains 'at the absolute forefront of what is possible' in terms of quality. The major risk is in a share price that values the enterprise at £123 million, about 21 times adjusted 2013 earnings. The earnings yield is just 5%.

Reject: Xchanging

stood still in terms of revenue and profit in the year to December 2013. It expects revenue to fall in 2014, but the company hopes to maintain operating profit in preparation for a return to growth in 2015.

Xchanging is a business process outsourcing company. It provides services to other companies - accounting, human resources functions, IT infrastructure and procurement, for example.

These areas of businesses are often neglected, and specialists such as Xchanging say they can conduct them more efficiently. In partnership with Lloyds of London, it manages claims for insurance companies, and it runs Gatwick Airport's networks, telephones and computers.

The company owns software that enables business processes and may give it a competitive advantage.

The company fell out of favour in 2011, when it lost major contracts and hurriedly disposed of a loss-making acquisition.

Thanks to this disposal, Xchanging now has little bank debt; it has also ended a number of joint ventures. The reduction in its reliance on large contracts and pursuit of a greater number of smaller contracts makes sense, but this strategy demands that it appeal to a broader range of customers.

Insurance is by far the most profitable niche. In 2013 Xchanging earned 38% of net revenue from insurance and achieved an operating margin of 22%.

Financial services earned operating margins of 9.5%, technology 9% and procurement 3%. It may be on its way to recovery, but Xchanging hasn't joined the watchlist. Because of its complex accounting practices and a changing business model, it has joined the "too difficult" pile.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

Editor's Picks