Share Sleuth's October Watchlist

9th October 2014 12:13

Each month Richard Beddard trawls through annual corporate results for his Watchlist and the Share Sleuth portfolio of companies that satisfy key valuation metrics such as earnings yield and return on capital - and profiles the most interesting candidates.

This week, he identifies the problems Air Partner is facing, including a waning demand for its military charters, after its summer profits warning.

The company is now tilting towards civilian work, such as running more corporate junkets and football teams.

Meanwhile, printhead manufacturer Xaar's dependence on heavy investment to stay ahead, the competitiveness of its markets and the faith required in its ability to develop new applications makes it a difficult company to love.

Air Partner

Air charter broker issued a profit warning in the summer, precipitating a crisis of confidence among traders holding the shares.

Although Air Partner is steadfastly profitable, profits are fairly volatile. The company charters planes on an ad hoc basis. Conflict and disaster are good for Air Partner, as companies and governments must ferry personnel, equipment and supplies to and from the afflicted areas at short notice.

Although the foreign policies of western governments are averse to conflict, at least by the standards of the previous decade, events are unpredictable and inevitably some years will be busier than others.

Air Partner is therefore trying to decrease its dependence on military charters, which are less in demand now that western governments have reduced appetites for war. Instead it's aiming to ferry more corporate junkets and football teams, for example.

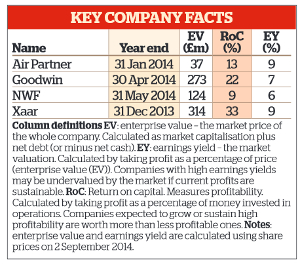

Perhaps unsurprisingly, management expresses confidence in the long-term future, and if it's right the current share price of 375p undervalues the company. It values the entire enterprise at £37 million, or eleven times adjusted 2014 earnings. The earnings yield is 9%.

Goodwin

full-year results revealed another year of strong and profitable growth. The company raised revenue 3% and adjusted operating profit 14%, as its mechanical engineering businesses still prospered from investment by oil and gas companies and performance at its refractory engineering businesses improved.

Goodwin manufactures valves used in oil and gas pipelines, rigs and refineries, liquefied Natural Gas tankers and terminals, and chemical, fertiliser, water and power plants. It also manufactures steel castings for the power generation industry, and large structures such as bridges.

About a quarter of revenue and 16% of profit in 2014 came from the processing of minerals used to cast jewellery, as well as from road aggregates, the fire-stopping mortar "Firecrete" and minerals for insulation.

Return on capital has been 22% in the last two years, although Goodwin warns that a slowdown in orders from oil and gas companies is likely to affect its results in 2016 unless it can increase market penetration.

In the short term there could be a repeat of 2011, when a petrochemical downturn coincided with increased investment in research and development and rising staff numbers to stymie profit.

Generally, though, Goodwin has been highly profitable for decades, and in the long term the company thinks the main driver of that profit - the average increase in energy consumption per person - is unlikely to subside. It has increased 50% in the past 50 years and the company reckons 80% of energy will still be from fossil fuels in 2035.

The likeable thing about Goodwin is that the investment case ties together. The company's objective is to build a sustainable long-term engineering business in growth markets by investing in quality, service and efficiency.

To invest year after year requires strong financing, and Goodwin has a cash surplus. It also requires strong management, and Goodwin is majority-owned by the founding family. Chairman John Goodwin has been a director since 1977, and managing director Richard Goodwin has been a director since 1981.

They've both been in their current positions since 1992 and they eschew short-term bonuses and incentive schemes; the long-term growth of their company has made them rich enough.

The products are technical, sometimes patented, and probably difficult to copy at an equivalent quality, and Goodwin has local sales and technical support staff to help customers.

Management could be wrong in its estimation of our dependence on fossil fuels, but as a diversified engineering company it can grow in other markets too.

A share price of £35.30 values the enterprise at just under £275 million, or 14 times adjusted 2014 earnings. The earnings yield of 7% is just on the wrong side of my 8% benchmark for a stalwart, a company capable of strong profitability through thick and thin, but it may well be the kind of company worth paying a small premium for.

NWF

Distributor full-year results describe business as usual for this relatively stable company. NWF manufactures animal feed and distributes it to farmers. Its sister businesses distribute ambient grocery products to supermarkets and food-service enterprises, heating oil to homes, and fuel and lubricants to businesses (including petrol stations).

A mild winter meant prices for heating oil and animal feed weakened, and compared to the previous year which was marked by a harsh winter, revenue fell by 1%.

Adjusted profit fell 11%. Cold winters help because they result in higher heating oil consumption and lower silage production (so farmers require more feed). Warm winters mean lower requirements for heating and animal feed.

Even so the company is still profitable enough to maintain its stalwart credentials. Profits are affected by commodity prices, but movements in one market can be mitigated by performance in another.

Profitability has been reasonably stable in recent years, at around 10% return on capital (including roughly capitalised operating leases).

Although NWF operates in commodity markets, it seeks to differentiate itself through superior customer service, for example by supplying fuel at short notice and adding value to animal feeds by increasing nutritional content and providing advice to farmers.

Scale may enable efficiencies. After acquiring SC Feeds in November 2013 it became the leading national supplier of ruminant feed (supplying one in six cows). But grocery distributor Boughey is regional and it's only number three in fuel distribution. The share price of 142p values the enterprise at about £123 million, about 16 times earnings. It's a bit pricey now, but remains one to watch.

Xaar

Although printhead manufacturer reported its full-year results in March, the share is in the spotlight because the price has plunged and may have thrown up a glaring value opportunity.

The share price has collapsed by more than 60% from its peak this year, to 420p. It fell 21% in one day in August after the company published half-year results.

Xaar rides waves of high revenue and profit as whole industries convert from analogue to digital printing. Digital printing is more efficient, particularly for shorter print runs and where an aspect of what is being printed is variable.

Xaar, which has been at the forefront of the conversion of ceramic tile pattern printing in recent years, first thrilled traders and then spilled them as that market matured very rapidly.

Xaar reports lower sales for ceramic tile printheads, now the main application for its technology, due to a slowdown in the Chinese construction industry and to lower prices as competitors have sought to ape its success.

Sales for other new applications like "Direct-to-Shape" have yet to materialise, although the company is confident they will. Direct-to-Shape allows printing directly on to non-flat surfaces like bottles.

Meanwhile, the company is expanding its factory in Huntingdon and increasing research and development, which will also squeeze profit.

Set against the gloomy short-term outlook, however, is the long-term prospect of Xaar repeating the trick it achieved in the middle of the last decade, when it partnered with printer manufacturers to digitise grand/wide-format printing (things like billboards and banners), and in recent years, when it led the way in ceramic tile printing.

Being at the forefront of digitisation gives Xaar a head start and, in the case of digital ceramic tile pattern printing, a leading position in the market, which it seeks to defend by improving its products and lowering prices.

In the short term profits will be pressurised as Xaar defends its market share and invests in Platform Four, but new applications of Platform Three, such as glazing tiles and printing laminated floorboards, plus the slow commercialisation of packaging applications, may help.

In the long term, profitability depends on its new Thin Film Platform technology. The company expects the first sales from Platform Four to be late in 2016, though. The mass conversion of the new markets it addresses, potentially fabric and commercial print, will take longer still.

A share price of 420p values the enterprise at about £310 million, 11 times adjusted 2013 profits. The earnings yield is 9%.

But valuing Xaar using record profits in 2013 would be reckless because they appear unsustainable. It's safer to assume future levels of profitability will be closer to their average in recent years.

On that basis Xaar may still be good value, but its dependence on heavy investment to stay ahead, the competitiveness of its markets and the faith required in its ability to develop new applications makes it a difficult company to love.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

Editor's Picks