Private equity star piles up the gains in Balanced Portfolio

8th December 2014 11:54

by Heather Connon from interactive investor

Share on

The past few months have been characterised by increased market volatility, especially during October, when markets sold off as doubt emerged that the US was strong enough to drive global growth.

However, once assurances were given that interest rates wouldn't rise soon, they quickly recovered. Markets were given a further boost when the Bank of Japan decided to increase its quantitative easing.

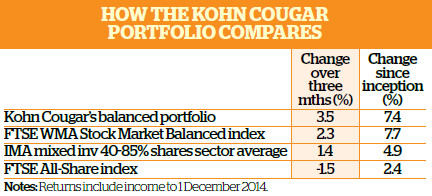

The portfolio had a good quarter, thanks to strong performance from several holdings. Roddy Kohn, principal of Kohn Cougar, says: "Being overweight global equity markets was of benefit, as was being overweight commercial property."

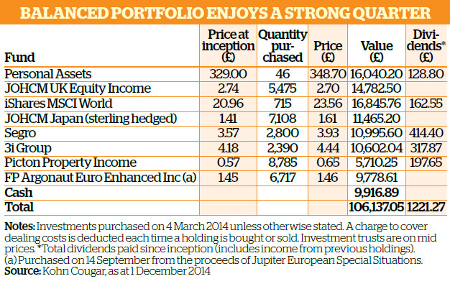

To view the balanced portfolio's holdings and trading chronology, click here.

Private equity strength

The strongest performance came from , the private equity investment company. It recently reported half-year results that highlight the progress it has been made since Simon Borrows took over as chief executive in mid-2012.

It has taken advantage of favourable markets to sell some smaller positions, and added three private equity holdings during the half year.

The company is to pay a dividend of at least 15p for the full year, reflecting its policy of distributing some of the proceeds from sales. This dividend represents a yield of 3.7%. Because of its size and liquidity, 3i tends to appeal to a wider range of investors than other private equity funds.

The second-best performance in Kohn's portfolio came from . The fund is managed by Scott McGlashan and Ruth Nash, who focus on small- and mid-cap Japanese companies and run a concentrated portfolio of 40-60 undervalued stocks with strong balance sheets.

The fund benefited from the rise in the Japanese market after the Bank of Japan's surprise announcement of an expansion of its quantitative easing programme.

But even before the bank's move, investors had received better economic news to reassure them: industrial production numbers suggested that the economy was coming out of its summer slump, and retail sales showed signs of recovery.

At the end of October the Japanese Government Pension Investment Fund announced its new asset allocation targets in favour of domestic and international equities, adding further fuel to the Japanese stockmarket rally.

Investor protection

But yen weakness meant sterling-based investors would still have lost money. Fortunately, investors in this fund are protected. Kohn says: "Because it is hedged to sterling, as the yen continues to weaken, it has benefited."

Both property companies in the portfolio increased in value. , a company that owns, manages and develops warehousing and light industrial property, benefited from demand for warehouses on the edge of cities to facilitate the delivery of goods ordered online. As a result, the company's rental income has grown and its vacancy rate fallen.

(click to enlarge)

Many property investment companies have been trading on premiums to net asset value for some time, and is on a 4.5%premium. As Kohn says: "Commercial property values are increasing, and there has been a market-wide reduction in voids."

The only negative performance in the portfolio came from , which fell over the quarter. However, Kohn has faith in the fund and its managers. "The long-term performance of Clive Beagles and James Lowen is excellent and we don't let short-term underperformance worry us," he says.

The other backmarker in the portfolio was , which rose by less than 1%. Its managers blame the sluggish European economy and worryingly low rate of inflation.

However, they say corporate balance sheets in Europe remain robust and that many companies will benefit from a weaker euro.

Kohn points out that the portfolio's performance over the quarter might have been even better relative to some other balanced investments, but for its lack of exposure to fixed income - or more specifically gilts, which had a strong quarter, aided by low inflation of 1.3%in October.

Its cash holding, at approximately 10%of the portfolio, was another drag, but Kohn remains comfortable with these positions.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.