Speedy Hire crashes spectacularly

1st July 2015 12:14

by Lee Wild from interactive investor

Share on

Seven weeks after presenting forecast-beating full-year profits, has warned of a slow start to the new financial year. That means results for 2016 will be "materially below" expectations and less than last year. Chief executive Mark Rogerson has quit the tool hire firm after just 17 months and City forecasts have, or will be slashed.

Speedy, whose shares slumped as much as 35% Wednesday to a two-year low, blamed a revenue shortfall on a lack of available equipment during the network optimisation programme, a focus on strategic accounts at the expense of SME customers, and poor customer service caused by disruption during the implementation of a new IT system.

"Whilst core hire trading across strategic accounts remains strong, without an improvement in revenue trend, and ahead of any delivery of the remedial programmes, the result for FY2016 will be materially below the board's expectations for FY2016 and the reported result for FY2015," warned Speedy.

Management has also failed to sell the remaining Oil & Gas business in the Middle East after talks broke down recently.

"There is no way to dress up the disappointment of today's update, an extremely frustrating turn of events which will test the patience of shareholders," wrote Speedy fan Andrew Gibb at Investec Securities. "We had believed the group had turned a corner; this statement reveals there is still much to be done."

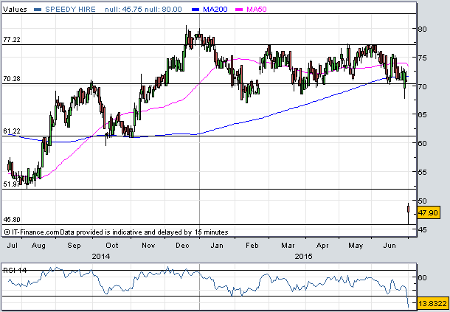

(click to enlarge)

The writing was probably on the wall after rival issued its own profits warning earlier this week. However, the departure of former Serco man Rogerson should be no surprise. Speedy's three main problems were management issues and were all avoidable. Chairman Jan Åstrand will run the business with new finance director and acting CEO Russell Down who will have both jobs until a replacement is found.

"This is extremely disappointing," said Åstrand. "I believe that Speedy remains a fundamentally good business but, whilst some progress has been made over the last year, the remedial action programmes have not been delivered as needed."

We'll get a further update in the last week of September, but already analysts have slashed forecasts. Gibb has cut earnings per share (EPS) estimates for the year to March 2016 by 38% to 2.4p, and by 25% for 2017 to 3.2p. At least net asset value (NAV) of 45p "should provide some support". The chart (see above) certainly appears to reflect that NAV right now.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.