Greggs offers huge upside after super summer

6th October 2015 13:26

by Lee Wild from interactive investor

Share on

Falling costs and rising sales during its third-quarter will continue to benefit for the rest of 2015. The high street baker says full-year sales are "slightly ahead" of plan and that opening more shops will help numbers against last year's strong fourth quarter. Having tumbled over 20% since their peak in July, Greggs shares are very much back on the menu.

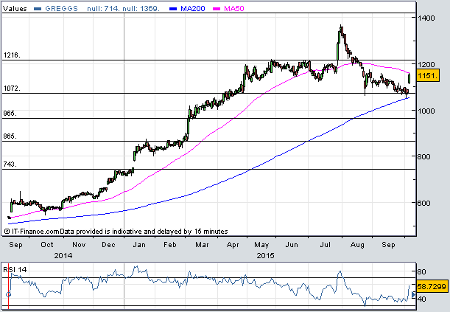

A series of impressive results had Greggs shares trading above 1,360p after this summer's interim results. At that price they were trading on a phenomenal 25 times forward earnings. Common sense prevailed, eventually, and a steady sell-off has seen the shares ease to 1,076p this week, kissing the 200-day moving average. But now, after a bullish third-quarter update, buyers are back and chasing the shares 7% higher Tuesday.

Like-for-like sales in its own shops grew by a larger-than-expected 4.9% in the 13 weeks to 3 October, a great performance given last year's strong quarter. So far this year like-for-like sales are up 5.6%. Total sales are up 5% and 5.1% respectively.

Crucially, more people are visiting Greggs these days and they're spending more each visit, too. Its healthier ranges are proving popular and its hot foods are back on the shelves as winter approaches.

And Greggs is busy updating its stores - 158 shop refurbishments have been completed so far this year and 200 will have received a makeover by New Year. Another 65 new shops have been opened, too, including 35 franchised units in places like Euro Garages. Overall, there will be an extra 50-60 Greggs in UK high streets this year. A new £13 million distribution centre in the south-east of England will also be up and running in the second half of 2016.

"Market conditions remain favourable with low cost pressures and a stronger consumer environment," says the firm. "We expect this to continue through to the end of the year after which increases to wage rates will drive greater inflationary pressure."

Nigel Parson at broker Canaccord thinks the share price slump gives investors "a chance for another bite". He upgrades earnings per share estimates for 2015 by 2.8% to 55.9p, and by 3.3% for next year to 60.3p. His rating goes up from 'hold' to 'buy' with a price target of 1,350p.

At the current price of around 1,150p, Greggs shares trade on 20.6 times forward earnings, dropping to 19 times for 2016. But it's this rating which has been a problem for many investors in the past. Indeed, it gave our own stockpicker Edmond Jackson palpitations back in March. But Greggs, it seems, is one of those stocks which now commands a high price/earnings (PE) ratio, and, just two years in to a five-year turnaround plan , it does deserve a premium rating.

N+1 Singer puts fair value at 1,400p, giving a forward PE ratio of 25 times 2016 estimates. It may well be worth it, but as we saw in July, stocks on high multiples are more vulnerable to a de-rating if either industry, or market conditions deteriorate.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.