Legal & General overcomes pension pain

4th November 2015 17:37

continued its recovery from the late summer sell-off with a decent set of third-quarter numbers. And it looks very much like a record year is on the cards, which should underpin the juicy dividend and a prospective yield of 5.6%.

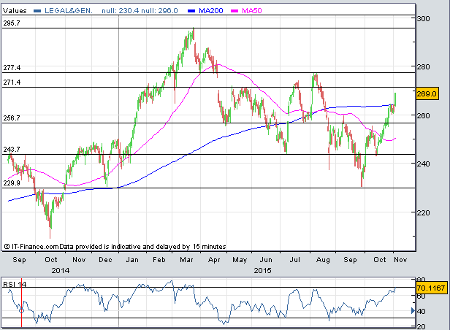

After making an all-time high in March, L&G subsequently lost more than a fifth of its value over the next six months amid concerns about global growth and Chinese troubles. The share price had since recovered and, after a couple of attempts in recent sessions, has smashed through its 200-day moving average. Following Wednesday's results, a 2% boost took the shares back up to 269p, taking gains to around 17% in just over a month.

But the good news doesn't have to stop there, says Panmure Gordon analyst Barrie Cornes, who still thinks they're worth 305p.

"The valuation is highly attractive based on 2015/16F IFRS PE multiples of 13.5x and 12.4x respectively," said Cornes. "In addition, we would highlight the cash generation that drives the dividend that already delivers a highly attractive 2015/16F dividend yield of 5.1% and 5.6% respectively."

(click to enlarge)

And these are attractive figures. Driven by its scale and international expansion, asset management did especially well with net cash growth of 14% to £943 million. Highlighting more rapid growth, net flows of £21.7 billion included mandates from the US, China, Korea and Taiwan, and took assets under management to £717 billion.

Now the 15th largest global asset manager, L&G's UK defined contribution pension assets total over £43 billion with its John Lewis mandate still to fund.

External net flows from its investment management division rose by 161% to £21.7 billion, annuity assets rose 8% to £43.1 billion and UK protection premiums were up 3% to £1.1 billion.

Annuity sales 'subdued'

However, sales of annuities did plunge by over 60% to £1.5 billion following major reform of the pensions industry. Looking ahead, management reckon individual annuity sales will remain "subdued", while investment management is on track to deliver £30 billion net inflows for the full year as the group continues to expand internationally.

"External political and regulatory uncertainties remain, but we believe that by aligning our strategy to macro trends we have created a high degree of resilience in our business model and are well positioned for further growth," said chief executive Nigel Wilson.

Even with market volatility and sector side solvency issues putting pressure on the money manager, Cornes reckons there is an investment case to be had.

"The share price has recovered in the last few weeks, having hit lows as a result of lower investment markets and (sector wide) Solvency II concerns," notes the analyst. "We believe that SII concerns will prove to be too conservative, but we note that insurers won’t get a response to the adequacy of their models from the PRA [Prudential Regulation Authority] until early December.

"We consequently believe that any weakness in the share price in the run up to SII should be seen as a buying opportunity."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Editor's Picks