Record-breaking GVC on a high

25th April 2016 13:29

by Lee Wild from interactive investor

Share on

has been an acquisitive beast these past few years. In 2013, the online sport betting and gaming firm paired up with to buy Sportingbet, and earlier this year it overcame stiff competition to snap up bwin.party for £1.1 billion.

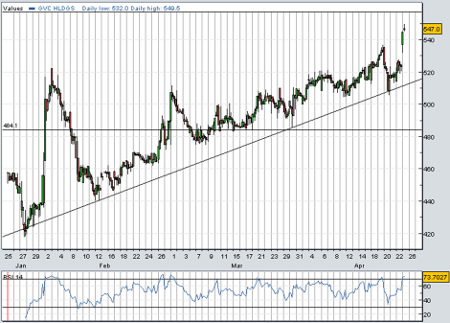

Management claim the business "has never been in a stronger position" and results for 2015 were certainly much better than expected. Even after hitting their highest since 2005, the shares do not look expensive.

We already knew net gaming revenue (NGR) rose for a fifth consecutive year in 2015, up 10% to €248 million (£193 million), or €679,000 a day - GVC said so in January. It jumped by 21% in the fourth quarter to €65.5 million.

Now, after a four-month wait, it's confirmed that cash profit - before tax, depreciation, impairments and a gamut of other one-offs - jumped to €54.1 million from €49.2 million in 2014.

That's a record and beats the range of analysts' estimates of €49.9-53.9 million. Assume bwin had been owned for a year, and pro-forma profit was €163.5 million - again, better than expected.

"A momentous year", chief executive Kenneth Alexander called it. "Not only has the company seen a fifth consecutive year of revenue and clean earnings before interest, tax, depreciation and amortisation growth, but the completion of the bwin.party acquisition in early 2016 affords us an opportunity to take the group to the next level."

It is if the first quarter is any indicator. Like-for-like NGR jumped 9% at constant currency, and the per-day figure is up 13% in the period to 20 April - GVC brands grew by 18% and bwin 11%.

Of course, getting the bwin deal done was not cheap. GVC raised £150 million from a placing and took out a €400 million loan from private equity group Cerberus to buy bwin, but it also incurred €23 million of acquisition costs; it's why reported profit before tax fell 38% to €25.5 million. Underlying profit jumped 21% to €50 million.

Simon French, an analyst at house broker Cenkos Securities, leaves his cash profit forecasts for 2016 unchanged at €197 million. But that still puts the shares on an enterprise value/cash profit multiple of just 7.5 times, a 26% discount to the gaming sector average of 10.1 times.

And French reckons GVC has the "best growth prospects and most diversified revenue base", which explains his 'buy' rating and 944p fair value, implying 73% upside, even after a 5% rally Monday.

Even away from the house broker, City analysts like what they see. Simon Davies at Canaccord likes the integration of the bwin sports book onto GVC's trading platform, and a return to growth at struggler PartyPoker. He tips the shares up to 615p.

Remember, there'll be a dividend holiday in 2016 - a condition of the debt financing to buy bwin - but GVC has been a generous payer in the past, and there's every reason to believe it will be next year. French looks for yield of "at least" 4.1% in 2017.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.