No end to Fever-Tree's growth spurt

8th November 2016 17:23

by Harriet Mann from interactive investor

Share on

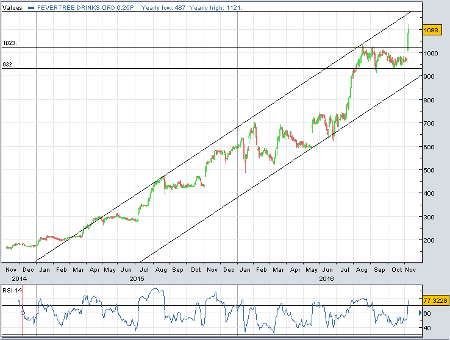

All it took was a seven-line update on Monday to spark latest rally, as the AIM market star surged 15% to yet another all-time high in just two trading sessions. This year's numbers will "materially" beat expectations, it said, extending the long-running upgrade cycle. Will the party ever end for this upmarket drink mixers supplier?

With less than eight weeks of the year to go, particularly strong growth in the UK means 2016 results should smash City forecasts. Driven by its core UK market, continued sales momentum has been complimented by new distribution wins. With some now expecting UK sales to double, a flurry of City upgrades have followed.

Shore Capital raised 2016 revenue forecasts by 9% to £94 million, implying 59% growth from last year. Pre-tax profit guidance increases by 15% to £31.6 million, nearly double 2015 profits, with 2016 earnings per share (EPS) now expected to reach 22.3p.

Upgrades spill over into 2017, with revenue of £110 million pencilled in, pre-tax profit of £34.9 million and adjusted EPS of 24.6p. Expect a full-year dividend of 5.5p this year and 7p next, giving a prospective yield of just 0.5% and 0.6% respectively.

Issuing just over 115 million shares at 134p, Fever-Tree floated at the end of 2014 with a market value of just £154 million. Fast-forward two years and the share price has just broken above 1,100p and the company is worth a whopping £1.3 billion. That's some rags to riches story, which puts the premium drinks maker on a similar pedestal to AIM darling .

Much like ASOS, the shares don't come cheap - although this is typical of high growth stocks. Even after Shore Cap's upgrades, Fever-Tree trades on 45 times forward earnings estimates for next year. That's dwarfed by ASOS on 67 times, although it represents a huge premium to soft drinks players like R Whites and Robinsons firm on 12.3 times, and Irn-Bru maker on 16 times.

As performance improves over the long-term, comparatives are toughening up. But Fever-Tree can still deliver upgrades, given its brand proposition and lack of competition, reckons Shore Cap analyst Phil Carrol. While lumpy distribution wins can provide opportunities to increase guidance, it also provides scope for share price weakness if performance falls short of expectations.

Management want to be sold in 55,000 UK outlets, but as they are currently only available in 10,000, there is plenty of room for growth. There are also plenty of opportunities in Europe and the US.

If a shock performance does provide temporary weakness, investors should view these as buying opportunities, reckons Carrol, pointing to the first half of the 2017 financial year as a period to be on the look-out.

"Whilst the group's PE ratio is high and well above its more mature soft drink peers in the UK, Fever-Tree is delivering growth that is significantly stronger and at higher margins than the peer group whilst generating strong cash flows and returns on invested capital. Taking this into account with the group's market opportunity, we reiterate our 'buy' recommendation," he adds.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.