These five blue-chip results cause ripples

2nd February 2017 12:45

by Lee Wild from interactive investor

Share on

It's been a mixed couple of weeks for London's heavyweight stocks. Maintaining the record highs reached mid-month was always a big ask, especially with maverick president Donald Trump signing executive orders for fun.

Since its 7,354 peak, the FTSE 100 is down over 250 points, or 3.5%, with big-hitters like and down 7% since Trump's inauguration.

And of the five blue-chips reporting results Thursday - Vodafone, AstraZeneca, , and - only the last two are up in the first two weeks of the Trump presidency.

Vodafone

And business isn't getting any easier for Vodafone. We hear today that service revenue grew 1.7% in the third quarter, in line with forecasts, but much slower than previous quarters. Italy and Egypt did OK, but the UK, Germany, Spain, India and South Africa were all short.

It did reiterate full-year guidance for the year to March 2017, which will be a relief given talk of downgrades heading into the numbers. However, growth in cash profit will now only be at the bottom of the range of 3-6%, or €15.7-€16.1 billion (£13.5-£13.8 billion).

There's intense competition in India, especially free offers from new entrant Jio, where Vodafone this week announced a possible merger of Vodafone India and Idea Cellular. Vodafone expects no let-up in the fourth quarter.

Reaction in the City has been mixed, but the sellers have it at the moment, sending the shares to their lowest levels since October 2014. They now trade on an enterprise value to cash profit (EV/EBITDA) ratio of 5.5 times, not expensive against a sector on 6.1 times, and offer a dividend yield of 6.6%.

"We think the shares have pulled back too far and VOD offers a calendarised 7.5% equity free cash-flow yield for 2017e rising to 10% in 2018e," says UBS analyst Polo Tang.

But John Karidis remains cautious about prospects at the current share price level. He's squiffy about potential for "irrational" competition in Europe, need for the mobile business to drive revenue growth, likelihood that Liberty Global is in no rush to strike a much more expansive deal with Vodafone, and further risks in South Africa.

"We think fair values will retreat to levels much closer to where Vodafone trades currently."

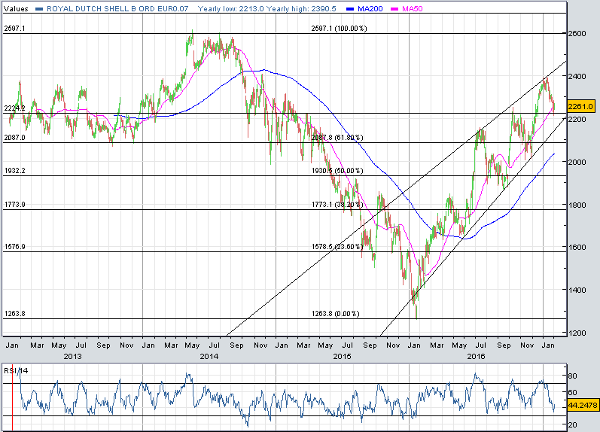

Royal Dutch Shell

On the flipside, Shell is going great guns. Agreeing OPEC production cuts - and getting members to keep their promise - has been a great feat, and has the oil price consistently at around $55 a barrel (£43.60).

That's good news for oil producers like Shell. So is news this week that it's sold $4.7 billion (£3.8 billion) of assets as part of a $30 billion disposal programme. It's now sold $10 billion of assets with a further $5 billion said to be in progress.

And fourth-quarter results, published Thursday, have been well-received, too.

A $0.5 billion tax issue was blamed for three-month earnings on a current cost of supplies (CCS) basis of $1.8 billion, up 14% year-on-year, but 36% below consensus estimates of $2.8 billion. But cash flow from operations of $9.2 billion smashed consensus of around $8 billion.

"We think the good cash generation and progress on disposals will help to offset much of the poor sentiment of the earnings miss," said Macquarie Capital analyst Iain Reid, who repeated his 'outperform' rating and £24.50 price target.

Compass

While the share price trend since the financial crisis has been upward for Compass Group, the caterer has spent the seven months since Brexit going sideways. It's failed to make a move above 1,500p stick, but this is the time of year it tends to outperform - it's why Compass made Interactive Investor's winter portfolio this year - and first-quarter results were decent enough.

Ahead of its AGM today at the home of rugby, Compass reported 2.8% growth in organic revenue during the final three months of 2016, down from 5% in 2016, but already well-flagged. Like-for-like sales "increased modestly" and the company is winning new business and keeping existing contracts.

Revenue in North America leapt 7%, offsetting a flat performance in Europe and 6.5% decline elsewhere as Brazil proved a toughie.

However, the weak pound has had a massive impact on numbers. Compass enjoyed a £924 million revenue windfall from sterling's post-referendum crash, and £74 million boost to the bottom line. Stay as it is, and revenue would receive a £2.3 billion uplift and operating profit £186 million.

Mark Irvine-Fortescue, an analyst at Panmure Gordon, pencils in pre-tax profit of £1.63 billion for the year to September, giving earnings per share (EPS) of 73p. 'Hold', he says, with 1,400p price target.

"We regard CPG as one of the most defensive companies in our coverage, with high quality compounding total return characteristics. The shares have edged back from recent highs and trade on 19x PE, 11.8x EV/EBITDA for FY17."

AstraZeneca

Compass's seven-month sideways trading channel pales into insignificance when compared to AstraZeneca. Its shares topped £48 for the first time in 2014, since when a short-lived visit to £55 last year was as exciting as it gets.

However, according to chief executive Pascal Soriot, 2017 has the potential to be "a turning point" for Astra as it nears the end of its patent-expiry period and brings new medicines to market.

"This year we have the opportunity to launch several life-changing medicines for cancer, respiratory and metabolic diseases," he says. "It is an exciting time as we rapidly approach the inflection point for our anticipated return to long-term growth, built on the solid foundations of a science-led pipeline."

Investors clearly need more convincing. Astra shares still trade near two-month lows, despite fourth-quarter and final results for 2016 largely in line with forecasts.

Three-month sales fell 12% at constant currency to $5.6 billion, but core operating profit jumped by 15% to $2 billion, about 5% ahead of city consensus estimates.

For 2017, chiefs guide for revenue to decline low-to-mid single-digit percentages, with core EPS seen down low-to-mid teens. Analysts had already figured that.

"The major uncertainty is the pipeline, but we think these results give some confidence that the current business is performing more or less as expected," writes UBS.

Johnson Matthey

Another company that historically does better during the winter months - it also makes our winter portfolio - Johnson Matthey delivered third-quarter numbers in line with expectations.

A weak pound flattered results at the catalytic convertor giant, with group sales up 19% at £876 million. At unchanged currencies the increase was a more modest 2%.

We're also told that underlying profit before tax was ahead of last year - current FX rates will boost operating profit by £65 million - and guidance for the full-year remains unchanged.

This implies pre-tax profit for the year to March 2017 of £485-£490 million, according to Deutsche Bank analyst Martin Dunwoodie. Consensus prior to these results was for just £469 million.

"The stock continues to look cheap at 14.7x forward PE (below its historical average) and is one of the few stocks in the sector to have de-rated whilst others have re-rated," argues Dunwoodie, who keeps his 'buy' rating and £37 price target, implying 13% upside.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.