Here's what'll haul Quartix shares into the 'buy' zone

24th March 2017 16:06

by Richard Beddard from interactive investor

Share on

Unlike the great partnerships, Buffett and Munger, , Apollo and Starbuck, I lack a sidekick. Sometimes I end up talking to myself...

OK, Richard, let's start with the fundamental question... How does Quartix make money?

Always a good place to start, Richard. designs and rents out vehicle telematics systems, little computers installed in cars and vans that track them and report back to the vehicle's owner or insurer using the mobile phone network. The current models are the TCSV11 and TCSV12, a miniaturised version of the TCSV11 that can be installed by the customer.

The circuit boards are manufactured in China and shipped to Quartix's supplier in Cambridgeshire for final assembly. The rental agreements are sold mostly by telephone from Quartix's main office in Newtown, and the devices are installed by 200 or so self-employed installers in the UK. The company also sells through distributors and employs two travelling salesmen who deal with bigger UK fleets.

So what makes Quartix special?

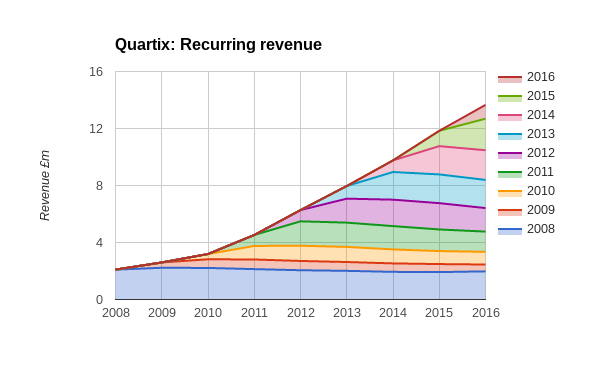

Glad you asked that. This chart says it all:

It shows how much of revenue earned from customers acquired in any particular year is retained in the following years by the core business, fleet operators as opposed to insurers (2008 is revenue from customers acquired between 2002 and 2008).

Quartix sold its first four units in 2001 and since then has rented out increasing numbers of units. Although the company does not generally lock in customers after the first year, it loses only about 10% a year compared to an industry average of about 15%. Every year the growing fleets of loyal customers almost make up for lost custom, while new customers grow revenue.

Growth has come entirely from the development and rental or sale of telematics systems and it's been achieved profitably. Return on capital is very high, and over the past six years profit has been matched by cash flow.

I get it, the product is increasingly popular and the company is converting that into big profits. How?

The simple fact is that as fleets grow from one or two vehicles to tens of vehicles, business owners can no longer keep tabs on them and employees become less productive.

Quartix targets white van man. Small businesses operate perhaps 1.5 million vans in the UK. A typical customer running a plumbing, building, office equipment, shopfitting or home maintenance business might operate a dozen vans. A low cost product that allows the fleet operator to check employees are on the job and driving safely appeals to businesses of this size.

Very large fleet operators demand bespoke features that are costly to implement and may not be relevant to other customers, so Quartix generally avoids the Eddie Stobarts, and refuses to pursue product developments that will not be adopted by at least 80% of customers.

I like the sound of low cost, tell me more

A simple product for a large group of customers is one part of the company's low-cost ethos, which starts with the founder and chief executive's modest salary, and extends throughout the firms direct marketing operation in Newtown, which is database driven. Quartix describes automation as “hugely important” and in the appointment of Ed Ralph as chief operating officer it sees an opportunity to improve further. Ralph was chief information officer at Abcam, another Cambridge based company that grew rapidly into a position of dominance by marketing antibodies to scientists.

Over the years, Quartix has derived economies of scale in research and development and installation by serving the fleet and insurance markets, while it has not relied on expensive field salesmen like many of its rivals.

Low costs may be a competitive advantage. Are there any others?

How about this: Quartix has a unique SafeSpeed database. While many telematics systems report when drivers break the speed limit, this is insufficient to determine that a vehicle is being driven safely. Quartix uses the 60 million data points it collects a day to work out the average speed cars and vans are being driven along sections of every road in the UK. The more a driver exceeds this average, the more likely he is to have an accident. A customer speeding at the 95th percentile is 20 times as likely to crash.

Monitoring safe speeds gives fleet customers reassurance their vehicles are being driven safely and economically and enables insurers to gauge risk, work out premiums, and educate younger drivers if they are driving badly.

You mention insurers, but Quartix is scaling back this business isn't it?

Yes. For six years now Quartix has sold devices to Wunelli (now part of LexisNexis), which supplies big insurance companies. Quartix doesn't say how profitable its two markets, fleet, which brought in 64% of revenue in 2016, and insurance, are, but it's always viewed fleet as the bigger opportunity.

The insurance market is, by-and-large, limited to newly qualified drivers who typically need the product for less than a year. Earning the vast majority of insurance revenue from one customer cannot be comfortable. Reading between the lines, it seems the more systems Quartix sells to Wunelli the less profitable incremental sales become, so it's paring them back.

While Quartix doesn't expect to cease supplying Wunelli, it's launched a new insurance platform that it hopes will win it more profitable insurance business from more diverse customers, for example high street insurance brokers who manage clients for small and medium-sized underwriters. Without telematics, the brokers could lose valuable customer accounts when they are unable to supply competitive insurance to the children of existing customers.

What are Quartix's prospects in the fleet market?

Pretty good. Last year, Quartix told me only about a third of 1.5 million fleet vans on UK roads already have tracking devices, of which Quartix had an 11% share, so it can keep growing in the UK. Then there's France and the USA, which are less mature markets where only about a sixth of fleet vans are fitted with tracking devices.

Quartix started supplying French fleets in 2011 and has been operating in the USA since 2014.

In France, Quartix has 10,000 vehicles under subscription, and the in USA it has 1,000. In the UK, where it has been operating since 2001, it has 72,000 fleet vehicles under subscription.

It's a one product company though. Isn't that risky?

It is, but if Quartix can keep recruiting more owner operators and earn exceptional profits, why would it divert its focus into potentially less profitable activities?

Maybe a company could come along with a better widget, but Quartix's widget does a good job, it's continuously improving, and a rival would not only have to develop that widget, but would also have to find a way of telling Quartix's disparate customers about it cheaply, and establish a cheap network of installers.

The elephant in the room may be self-driving vehicles. Without drivers, Quartix has no market, but that seems a long way off when you consider Quartix's customers. They aren't plying motorways in convoys, they're navigating City and residential streets. And, unlike a delivery or taxi service, the driver, the plumber, or electrician, needs to be in the car any way. Until the technology has been refined to the point it's significantly safer and cheaper than a vehicle with a telematics system, they might as well drive themselves.

So should I buy the shares?

Ah, it was going so well... This is where things get really tedious.

Chief executive Andy Walters is an exemplary founding entrepreneur, frugal in many respects, but not in terms of investment to meet customer needs in profitable niches. One of the endearing things about him is his aversion to hype.

He won't be drawn into labelling SafeSpeed a big data project, or tracking devices as part of the Internet of Things. He resisted calling Quartix a telematics company until convention made it essential. Vehicle tracking was a good enough descriptor.

I think the odds are heavily in favour of the company living long, and prospering.

And that's what the market's betting. Quartix's earnings yield is 3%. We're paying 33 times profit in 2016. There are a lot of cheaper companies out there.

The comparison is unfair. Aside from Quartix's superior growth prospects, it lost $1 million in the USA last year, where it has eight sales and marketing people. Starting up there is expensive. Installers have to cover a much larger area, sometimes to install demonstration units, although the self-installed TCSV12 may offer a way around that cost.

The USA is closing down its 2G network, so Quartix has to use more expensive 3G modems, which is buying in relatively small quantities. When it scales up, Quartix expects the investment to pay for itself many times over, but currently it's reducing the underlying profitability of the UK business (France is small but profitable). If Quartix halted its US expansion, the shares would instantly look cheaper, but that would probably be a very bad idea.

Also Quartix doesn't capitalise development expenditure, an accounting practice that would enable it to defer development costs and boost profit now.

My Decision Engine ranks the company 7/10.

I love Quartix, but I hate its valuation. Fiddling around with the assumptions behind the valuation, ignoring the drag of the US operation, and capitalising some of the development costs, might just haul it into the 'buy' zone.

A year after I climbed up onto it, I'm sat uncomfortably on the fence. The heart says yes. The head says yes and no!

Richard, I want to cry.

----

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.