Model Portfolio review: All change as soaring funds skew the balance

14th July 2017 16:07

Strong performance, introducing targeted regional exposure and weeding out weaker funds means nine of our 12 model portfolios are adjusted in this quarterly review. Andrew Pitts and Holly Black explain why.

A stronger pound and a shock general election result couldn't hold our model portfolios back over the past three months. As stockmarkets have soared, some of our holdings have rocketed and thrown our portfolios slightly out of kilter. So, it's all change this time around as we rebalance and regroup, ready for the next quarter.

Just three of our 12 model portfolios have avoided any changes at this quarterly review. While we adopt a buy-and-hold approach and try to keep trading costs to a minimum, some of the weightings in the portfolios need adjusting and we are introducing exposure to Europe and Asia for two of them.

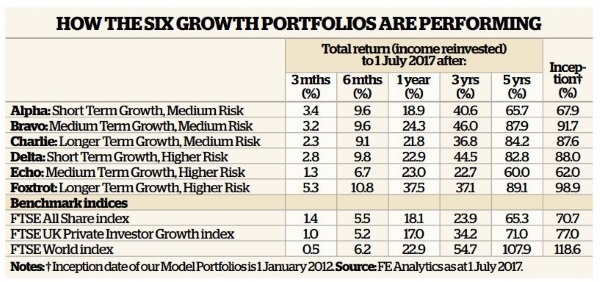

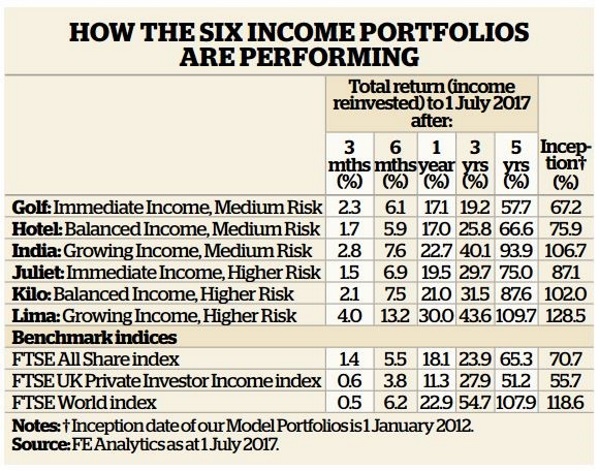

Every one of our portfolios beat their FTSE Private Investor index benchmarks over the past three months and all bar one beat the FTSE All-Share index; with our higher risk options, Foxtrot (longer-term growth) and Lima (growing income), leading the way with returns of 5.3% and 4% respectively over the period.

Kilo, the higher-risk balanced income portfolio, has become the latest to join the '100% club', while Lima and India have returned 129% and 107% respectively since inception in January 2012. Foxtrot has now returned 99% since our portfolios were launched so could join the club by the time of our next review.

Growth portfolios

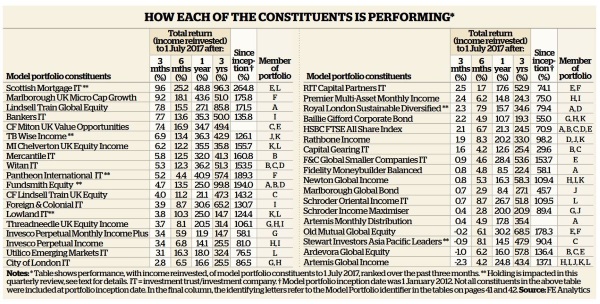

Starting with our growth portfolios, the first change we are making at this review is to reduce our allocation to in Alpha, the medium risk, shorter term growth portfolio. Terry Smith's flagship fund has delivered stellar performance, up 25% over one year and 100% over three. But that success has skewed its weighting in the portfolio and it now accounts for almost 25% of assets, which is too much.

With that in mind, we are reducing our holding by 5 percentage points and redirecting that money into , a mixed asset fund. The fund is up a healthy 7.9% since we introduced it in January and currently only accounts for 11% of the portfolio.

features in three of our portfolios currently but, after some disappointing recent performance, we are removing it from two. The fund, which is down 0.9% over the past three months, will remain in Charlie. We feel it still suits the strategy of this longer-term, medium risk portfolio and it is important to remember the fund's impressive track record, up 81% over five years.

For the higher-risk portfolios, however, we think there are more suitable options. We are swapping the Stewart fund for in Delta, and this shorter-term growth portfolio will benefit from the investment discipline that a focus on yield entails.

It's a relatively new fund, launched in March 2016, but is run by Jason Pidcock who has a strong track record in the sector, having steered a steady course of gains for the fund for almost a decade. His new fund currently yields 3.8%, much higher than rivals.

Its largest country weighting is to Australia, where it has 21% of its assets, with a further 20% in Hong Kong and 14% in Taiwan. As well as investments in electricals and technology companies such as Samsung Electronics and internet group Tencent Holdings, the fund has 13% of its assets in real estate.

In the medium-term Echo portfolio, meanwhile, we are opting for . It's arguably a riskier option but manager Ezra Sun has generated strong performance over a number a years and the fund has been a winner in our annual awards for the past two years. In a further link to Newton, Sun ran the firm's Asian funds from 1995 to 2004.

Echo was the weakest performer of our growth portfolios over the past quarter, returning 1.3% over the period, though it still comfortably outperformed its benchmark, the FTSE UK Private Investor Growth index, which edged up 1%.

In a major shake-up to Foxtrot we are bringing in some direct exposure to Asia – currently only around 8% of the longer term growth portfolio's assets overall are in the region. To do that we will reduce the portfolio's private equity holding , which currently stands at 21.8%, shaving it by 5 percentage points to just under 17%.

We will also be selling – the trust has been strong over the past 12 months, producing a return of more than 35%; many mining giants have seen their profits boosted over the past year because they get a high proportion of their earnings from overseas, so their bottom line gets a kicker when those earnings are transferred back when the pound is weak.

But, with so much uncertainty in the sector, the trust was the worst performer of all our portfolio constituents over the past quarter, down 2.8%.

The profits from the two sales will be funnelled into the trust. The First State Stewart Asia-managed trust focuses on companies with a market capitalisation of less than £1 billion and its biggest weightings are in consumer stocks such as Indonesian department store group Mitra Adiperkasa.

Some 28% of the trust's assets are in India with 13% in each of China and Taiwan.

This addition should help bring some extra diversification into the portfolio and tap into some of the growth in Asian markets.

In a second change to Foxtrot we are also switching from the , which has been in the portfolio since inception, to the fund. The active fund's performance has been far superior to the tracker fund, with returns of 184% versus 105% respectively over five years. Richard Watts' fund has 43 holdings, compared with 254 in the index, so it's a more concentrated choice. His biggest investments include online retailer and payments company

Domestically focused companies were hit hard after Brexit as it was feared a weaker UK economy could hit their profits, but many have now started to recover. We feel that with so much uncertainty on the horizon as Brexit negotiations play out, an active manager will be better able to respond to any challenges or opportunities which arise among medium-sized companies.

Bravo, the medium-term, medium risk growth portfolio escapes any changes in this review. It is up 3.2% over the past quarter and is edging towards the 100% club with a total return since inception of almost 92%.

Income portfolios

We introduced our UK property investment trust, , in the October review, following the post-EU referendum strife that saw dealings in our holding of suspended, as were many other open-ended funds in this sector. The trust has since gained 22%, and its share price discount to net asset value has fallen from a chasm-like 24% discount a year ago, to a premium of almost 6% today.

A constituent of the immediate income Golf and Juliet portfolios, F&C Commercial Property still provides a decent 4.1% yield despite its premium rating. Existing investors may wish to stick with the trust, but for new investors, we are switching to , a trust with a similar yield but which is trading on a more reasonable premium of around 2%.

Hotel and India, the medium-risk, balanced and growing income portfolios, have escaped any changes in this review, but we have been disappointed by the recent performance of Mark Barnett's fund in both of these portfolios.

The fund has underperformed its peers over the past year, returning 14% compared to the average of 19% for similar UK equity income funds, and is only in line with the average fund in that sector over three years. Barnett says energy stocks in the portfolio had been hit by the Conservative manifesto pledge to cap prices in the industry, which has since been quietly dropped.

For now, though, the performance of the two portfolios is holding up well. Hotel has climbed 1.7% over the past quarter and India by 2.8%.

For the higher-risk, balanced income Kilo portfolio, we have made the decision to sell investment trust, which has underperformed its peers lately, up just 2.4% over the past quarter, and is in the bottom quartile of its sector over 12 months. The firm has now recruited BlackRock's Mark Wharrier to join the team, which could perhaps help shake-up performance.

Nevertheless, we have decided to move the 17% of the portfolio we held in Troy into , a global multi-asset fund which has solidly outperformed over the long-term, and is in the top-quartile of its sector over both one and three years.

The fund already features elsewhere across our range of model portfolios and has returned a meaty 6.9% over the past quarter, putting it among our top performers for the period.

Lima, our best-performing portfolio with a 129% gain since inception, has been propelled forward by the impressive performance of trust. Up an eye-watering 264% since inception and the top performer of all our portfolio constituents, the fund now accounts for 25% of this higher risk, growing income portfolio.

Such success has had a dramatic effect on the Lima portfolio, which is our second strongest performer over the past three months with a 4% return and the best of the bunch since the start of the year. It is our strongest performing portfolio since inception, with a return of 128.5%.

Scottish Mortgage has a small but growing dividend (which it has raised for 34 consecutive years), which matches the ethos of this portfolio. However one of the reasons we included the trust in Lima was as a potential source of capital withdrawal for investors, in the event that income disappointed from other holdings.

So for the purposes of the model portfolio we are reducing its weighting to Scottish Mortgage by 8 percentage points to just over 17%, and will also be reducing our UK exposure by ousting Troy Income and Growth from the group too, freeing up around 23% of assets.

We are replacing the Troy fund with some exposure to continental Europe via income shares (the trust also has a growth portfolio). The trust, which currently yields 3%, focuses on large companies but also targets growing, medium-sized companies in the region.

It is one of three Europe-focused trusts which have returned 40% over the past year, has also beaten its benchmark in each of the past five years, and has the added bonus of trading at a 6.5% discount to its net asset value.

The proceeds from the Scottish Mortgage sale, meanwhile, will be split equally between and trusts, which previously had comparatively low weightings in the portfolio, but will now each get an extra 4 percentage points, to just under 13% and 14% respectively.

The summer months can be a difficult time for investors; lower trading volumes mean there can be some volatile swings in the market and there is much uncertainty to come with Brexit negotiations, rising inflation and speculation about whether central banks will raise interest rates. But our portfolios are well-diversified and are holding up strongly. There are some holdings we are keeping an eye on, and those which continue to disappoint us could find themselves ousted come next quarter's review.

Buying the model portfolios

Customers of Interactive Investor, Money Observer's sister website, can purchase a Money Observer Model Portfolio for an all-in cost of £10 (plus applicable stamp duty where a portfolio holds investment trusts).

In the past, their investment was split equally between each portfolio's constituents. However, on model portfolios purchased since 8 July 2016, Interactive Investor allocates the investment in line with each constituent fund's weighting within the model, as at the last quarterly review.

This will help to ensure that the performance of any new investment will more accurately follow the performance of the selected model portfolio(s). As was previously the case, customers will be alerted to any changes that are made to the portfolios at the quarterly review point, and should they choose to adjust their existing holdings in line with the information provided, the usual dealing charges will apply.

This article was originally published in our sister magazine Money Observer. Click here to subscribe.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise.The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Editor's Picks