June signified a great deal more than just the end of May

28th July 2017 13:15

by Andrew Pitts from interactive investor

Share on

If a week is a long time in politics then the three months since this column last appeared has been an eternity. And what happens next has potentially profound consequences for savers and investors.

The "strong and stable leadership" promised by Theresa May when she announced the snap general election will go down in political folklore as a classic example of hubris.

Where May has failed, Labour leader Jeremy Corbyn has succeeded, not only in defying political pundits who predicted he would lead the party to electoral oblivion but also in confounding the large majority of Labour MPs who last year said they had no confidence in him as leader.

Labour has leapt in the polls from more than 20% behind the Tories in late April to roughly 5% ahead in early July. A YouGov poll for The Times on 6 July had Labour on 46% and the Conservatives on 38% of the vote.

Compounding Tory woes are YouGov's ratings of the respective party leaders, which have reversed since the election was called.

In late April Theresa May had a healthy net favourability rating of +10. Following the election, it had plummeted to -34.

"The prime minister is currently about as unpopular as Jeremy Corbyn was in November last year, when he scored -35. In contrast, his net favourability score is +0 - meaning that as many people now have a favourable view of him as have an unfavourable view," YouGov reports.

The attractions or otherwise of the respective leaders has restive Tories wondering how long it is best to keep the lame-duck premier in power before she, presumably gratefully, falls on her sword in favour of a leader the electorate finds more palatable.

The breezy Brexit secretary, David Davis, is being touted as a contender, but don't underestimate the chances of "spreadsheet Phil" Hammond.

Much like when John Major was surprisingly picked to replace Margaret Thatcher as leader, the ex-foreign secretary and current chancellor is perceived as something of a "grey man".

But as the next critical stage of Brexit negotiations gets under way in the autumn, Tory grandees may conclude such qualities could play well with the electorate.

Hammond would be a popular choice among UK business leaders, as he clearly has a "softer" view on how Britain should leave the EU and how long the process should take.

The current parlous state of the UK's Brexit negotiations aside, the fact that the Conservatives are plundering Labour's election manifesto for voter-friendly policies clearly shows they have few, if any, of their own.

May's recent call for other parties to "contribute and not just criticise" on a range of policies, in a bid to shore up her government via cross-party consensus, has drawn predictable scorn.

These are clear indications that voters could face a fresh general election before the year is out. "September would be nice," says Corbyn. That would not give a new Tory leader much time to put their own stamp on the party and formulate policy to win back trust and votes.

Early election or not, it would be surprising were the Tories not to adopt some watered down wealth-redistributive ideas from Labour's hymnbook that have clearly gone down well with voters.

When it comes to the current tax breaks available, for savers and investors, it's a case of "get it while you can". Pension tax relief, for example, costs the Treasury a net £21 billion a year, so I can't see higher-rate tax relief on pension contributions being available much longer, and the £40,000 annual limit on contributions is also under threat.

The same can be said for the annual tax-free Isa allowance of £20,000. Both sets of reliefs and the contribution limits are widely viewed as benefiting those savers and investors who need them the least.

To further redress the balance between the haves and have-nots, both political parties would likely adjust the capital gains tax regime to varying degrees. Currently, capital gains of up to £11,800 a year are free of tax, while gains over this amount are taxed at 10% for basic-rate taxpayers and 20% for higher-rate taxpayers.

In the event that the minority Conservative government clings on to power, I would expect watered-down redistributive measures in the next Budget. But shorn of its centrist influences, an overtly left-wing Labour government would be expected to hit the comparatively well-off where it hurts, not only on the tax breaks above, but with inheritance tax thresholds too.

June swoon suggests a tumble to come

Meanwhile, stockmarkets here and globally are taking the seismic political events in the UK in their stride. In any case, from a global perspective, what happens in the UK is something of a sideshow.

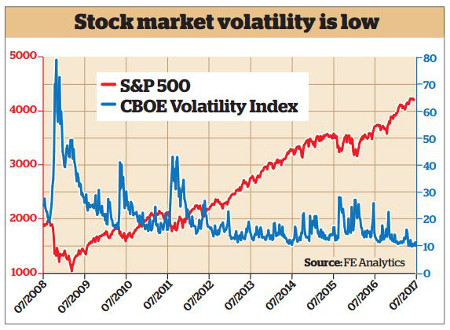

However, some worrying signals are emerging in bond and stockmarkets. For some time now stockmarket volatility has been distinctly lacking. Any signs of market weakness have been swiftly leapt upon by investors "buying the dip".

In the all-important US market, the CBOE Volatility Index has been hovering between around 10 and 12 for some months.

It means Wall Street's so-called "fear gauge", which provides a numerical number indicating how relaxed or horrified investors are about prospects for constituents of the S&P 500 index, is at its lowest average level in its 24-year history.

The "easy money" created by quantitative easing (QE) and ultra-low interest rates is responsible for this phenomenon, rather than any credible evidence that suggests prospects for equities are better than at any time in the past quarter century.

Caution required

Although history shows that stretched valuations can be maintained for longer than justified by a market or stock's fundamentals, investors need to be on guard.

It is widely acknowledged that there will be a price to pay one day for the bounty that QE has bestowed on investors in both stocks and bonds.

That day could be drawing near. Alberto Gallo, head of macro credit strategies at London-based Algebris and manager of the Algebris Macro Credit fund, points out that poor-quality US mortgage debt heralded the onset of the 2008 financial crisis and that QE helped avoid an even deeper recession, "but it didn't solve the root cause of the crisis".

The root cause is a bigger problem today because global debt has risen an astonishing 276% in the past decade to $217 trillion (£168 trillion), or 327% of global GDP, states the Institute of International Finance.

Writing for bloomberg.com, Gallo reckons that the "biggest worry for investors is that the calm environment established by QE may conceal a storm, and that such extraordinary measures may have encouraged the formation of asset bubbles ready to pop when loose monetary policy ends".

"Unlike in 2008, the culprit isn't low-quality subprime mortgage debt, but sovereign bond markets."

That period of calm looks to be over. The first signs that the QE foundations underpinning bond and equity markets are cracking came towards the end of June.

The US Federal Reserve had raised interest rates (which was widely expected), but it also then outlined how it would start to decrease the size of its $4.5 trillion balance sheet by tapering (not reinvesting) in the securities it had previously bought under QE.

This caused a mini "taper tantrum", not just in sovereign bonds, but in equities too. The hawkish tones from the US Fed have since been echoed by central banks in the UK, Canada and Japan, and by European Central Bank governor Mario Draghi.

Draghi said the ECB will outline plans to curtail its QE asset purchase programme in the autumn. That caused another short storm in global bond markets that reverberated through equities and currencies too.

When devising their investment strategy today, investors should not ignore these early warnings.

But several others should also help focus minds. According to Longview Economics, the US stockmarket is now in its second-longest and third most-profitable bull market period since 1896.

The US market is trading at its highest cyclically adjusted price earnings (CAPE) ratio since before the 1929 Wall Street Crash and the late 1990s TMT boom.

"What we can be sure of is that, as this bull market continues and valuations ratchet ever upward, the risk/reward becomes more skewed to the downside," states the investment team behind the .

"The longer-term returns investors should expect at current valuations are now very low indeed, and reversion to a more 'normal' earnings multiple would be likely to herald a significant drawdown."

In this post-crisis era when the actions of central bankers determine the direction of travel for financial assets, it is perhaps not so odd that the improving global economic conditions that have prompted them to consider withdrawing QE could be the catalyst that brings asset prices crashing down.

We need to watch the bond markets very closely over coming months for further stress, because this would undoubtedly spill over into equities. That is probably more important to most investors now than the likely curtailment of tax breaks, to varying degrees, by the UK's warring political parties.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise.The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.