Tactical Asset Allocator: Emerging market exposure on the up

21st August 2017 10:38

by Ceri Jones from interactive investor

Share on

The recovered lost ground over July, moving back up to its mid-June levels, but fell again recently as the US-North Korean stand-off intensified and investors fled to safe havens such as gold and the yen.

No one yet believes a nuclear conflict is likely and we have seen similar posturing between Donald Trump and Kim Jong-Un before. Markets are therefore likely to bounce around in line with the rhetoric in the next few months, but any indication of a deepening crisis would cause carnage in the markets.

Trump's credibility is now at an all-time low and his utterances increasingly make-believe and distorted.

The administration's vacuum on key policies such as lower corporate taxation is a rather more prosaic concern than world war, but the way Trump frequently pulls figures out of the air when talking about his plans suggests that these policies have yet to reach the drawing board.

Ironically, his election promises that have been more effectively implemented - immigration and import controls - will both damage US productivity.

Before the feuding with North Korea became so heated, the Dow Jones index had enjoyed a strong run, posting nine straight days of gains in late July despite uncertainty about the strength of the dollar, which has already fallen around 10% this year.

Rate rises loom

Business confidence is robust, leading to the possibility of further Fed tightening in the near term. The Federal Open Market Committee (FOMC) voting member Neel Kashkari was the only member to vote against the June rate rise and has been urging caution until inflation firms, despite the surprisingly strong gain in July job growth.

The next big milestone will be the Jackson Hole symposium at the end of August, when we will hear the latest views of central bankers and policy experts.

Stockmarket growth over July was less pronounced in the UK than the US, but still evident, with the mining sector performing well on the back of stronger iron ore and steel prices.

New Chinese regulations curbing steel capacity in the winter months have encouraged buyers to push their demand forward, driving Chinese steel futures to their highest levels in more than four years.

Uncertainty over Brexit also looms large and optimism has been tempered by the realisation that it is hopeless for Britain to take anything but a highly competitive pro-business stance to protect the economy in the years ahead, and worse - that this is patently not a vision shared by chancellor Philip Hammond.

UK investors have also been shifting their portfolios in anticipation of higher borrowing costs, as the Bank of England turns increasingly hawkish and opinion between the rate-setters begins to gape.

Inflation has stayed in check and is forecast to peak around 3% in October before falling back next year. This should give the BoE some breathing space, but the timing is hard to gauge given the Monetary Policy Committee's (MPC's) hints that the bank could hike sooner than expected.

Two members of the MPC voted in favour of a rate rise in August, down from three in June following the departure of hawk Kristin Forbes. However, in a BBC radio interview, deputy governor Ben Broadbent suggested the economy could cope with a small rate rise, as unemployment is at a 40-year low and wages are expected to rise.

The Bank must be painfully aware that if it does not raise rates in the next six months, its opportunity to stimulate the economy will have passed.

The immediate risk to investors is a bond market rerating; but crucially, higher deposit rates would also help prevent a speculative bubble in limited risk assets such as infrastructure and P2P, which have become sought-after assets in a universe where there is very little choice.

Many UK headlines have focused on the plight of the UK equity income fund sector, where popular dividend-paying shares such as and have fallen on poor drug trials and additional regulatory constraints respectively.

The Investment Association (IA) sector is heavily concentrated in a few mega-shares, and popular funds such as have suffered.

Income investors should probably look again at smaller dividend-paying companies, global equity funds, emerging market bonds and property, where inflation-linked rentals offer some protection.

High-yield emerging market bonds cover a very broad range of regions, currencies, types of economies and credit profiles, and offer a higher average credit quality than their US equivalents.

Furthermore, the indices that cover emerging market high-yield corporates have a lower sensitivity to interest rates than broad developed nation high-yield markets.

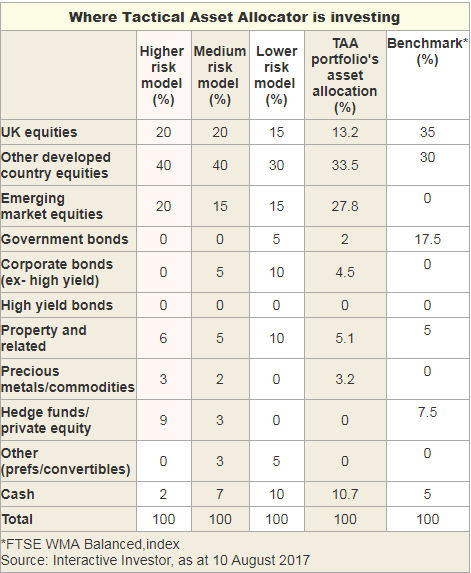

Our portfolio is overweight to emerging markets at nearly 28% and, despite the uncertain political climate, a high allocation to these markets remains the most attractive long-term opportunity for generating growth.

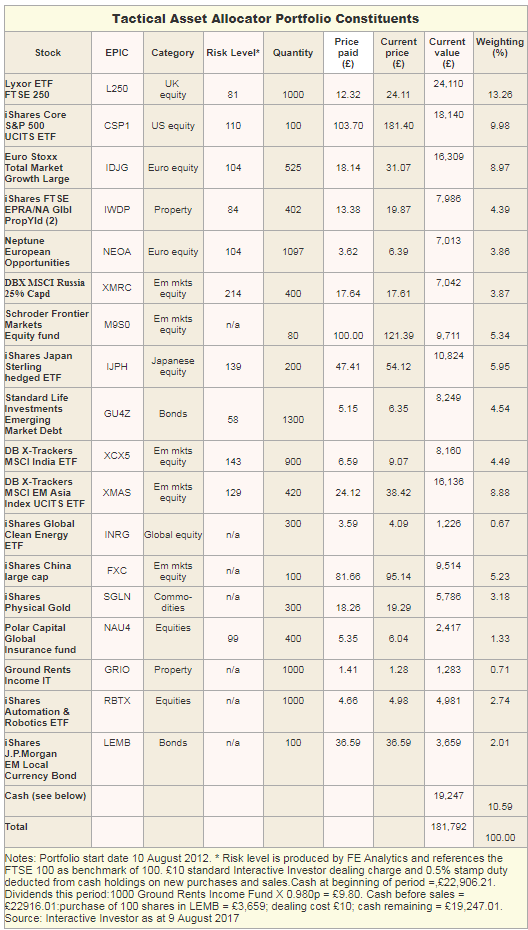

However, it does mean that instead of buying EM corporate bonds, we are going to allocate cash to an ETF focused on EM government bonds, the iShares JP Morgan EM Local Currency Bond ETF (LEMB), which will help diversify the portfolio beyond the EM corporate world.

If the US is now a nation where little of what officialdom says about the economy can be trusted, China's thrust is the other way, towards greater openness and transparency.

Despite events such as the circuit breaker put on the Chinese A-share market in January 2016, and capital controls subjecting foreign transactions of more than $5 million to mandatory pre-screening by regulators since November, China is engineering a capital markets revolution.

The opening of the Shenzhen-Hong Kong stock connect last year, and the recent inclusion of Chinese A-shares in the MSCI index in June, mean that long-term globally diversified investors should be sure to set an appropriate allocation to the country.

Gold prices have already been pushed up by tensions between the US and North Korea, most starkly after Kim Jong-Un responded to warnings from Trump with a threat to strike the US territory of Guam.

There may be more spikes to come if the conflict intensifies, but most of the upside is already in the price.

Although we have become accustomed to talking about gold as a "store of value", as a long-term hold it is generally disappointing, useful only to cover sporadic episodes of plummeting market sentiment.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.