Nick Train: The bull market is here to stay

6th September 2017 11:21

by Kyle Caldwell from interactive investor

Share on

For almost a decade financial markets have been climbing the proverbial 'wall of worry', despite the fact that since March 2009, when markets bottomed out following the financial crisis, share prices across a broad spectrum of sectors have edged higher and recovered their poise.

Indeed, far from investors popping the champagne corks and partying like it's 1999, the current eight-year-long bull market may well possibly go down as one of the most unloved in history. Irrational exuberance, common during other stockmarket purple patches, has been noticeably lacking. Instead, there's a feeling of distrust in the air, with investors sceptical as to whether the rally has been built on solid foundations.

These concerns are understandable, as there are various threats on the horizon that could derail the bull market: Brexit, a Donald Trump tweet, North Korea, to name just a few. But arguably the biggest unknown is how stockmarkets will react when the money printing stops.

Don't blame it all on the easing

Since the crisis, unorthodox monetary policy has been present in the form of ultra-low interest rates and large doses of quantitative easing (QE). While there's debate over whether QE has achieved what it set out to do – stimulate the economy – the big fear as far as investors are concerned is that the policy has distorted stockmarket valuations, and as a result has helped send share prices to elevated levels that will ultimately prove unsustainable.

Nick Train, one of the UK's most respected UK stock pickers and a manager who has seen a fair few market cycles during his 30-year career, is not losing any sleep over this doomsday scenario playing out, however. In fact, on the contrary, Train is of the opinion that QE's impact is not 'demonstrable' and instead argues that the bull market is "only just getting started".

"If QE was having so much of an impact then why does , a share that has not cut its dividend since 1945, have a dividend yield of 7%? If there's QE then surely Shell would be yielding 2%. That's my take on QE and why it doesn't worry me," says Train.

Central to Train's bullish stance is the technological boom, which he says is "10 years old and has only just started getting going". He adds: "I do think we are at the beginning of a fully-fledged bull market in digital technology. It is 10 years young, and when you look back at history some bull markets lasted a very long time. The railway rally, for example, lasted 50 years."

There's one caveat, however. While Train believes that a minute spent thinking about the possible implications of Brexit or what Donald Trump will do next is a minute wasted, he says a meaningful slump in global trade would concern him.

Train's two UK portfolios, and , have around a third of assets invested in either out-and-out tech companies such as , or companies that are radically improving productivity via technology, with one example being stockbroker .

The rest of the portfolios consist of consumer goods and services firms that are dominant players in their respective markets: , , and are four of the 25 names in FGT. Corporate longevity is key: the vast majority of holdings were founded more than 100 years ago.

"I do not think my investment approach is anything more sophisticated than saying: I like to invest in companies that do stuff people can't live without. This could be products that taste good, or a product that holds people's attention. Over the long term these are the businesses that have survived and will continue to thrive in the decades to come."

He adds that, overall, most businesses have too many flaws to invest in, and that therefore over the long term "the majority of quoted companies don't last very long". This is perhaps why, with an average holding period of well over a decade, he seldom trades.

Two years ago, however, was a busier period than usual, as Train introduced a new company into the portfolio – premium drinks firm . This was the first new holding in four years. "It has become harder to find companies that will not be knocked off their perch," he acknowledges.

He adds: "I know it is rather clichéed to say "one of my favourite Warren Buffett quotes is....", but one of his principles I particularly like is that the best new ideas are often old ideas. Things go in and out of favour, so rather than buying something new, there are always opportunities to top up existing positions."

One area Train has been adding to lately is the three financial services companies he owns – , and Hargreaves Lansdown – on "share price weakness" following the recent publication of the Financial Conduct Authority's (FCA's) long-awaited asset management market study. The tone of the report was critical, with the FCA raising concerns that the industry enjoys "high levels of profitability".

Train, however, thinks that although the pressure has been raised on fund managers to reduce fund charges, lower fees would not necessarily mean that profit margins would decline or fall commensurately.

He adds: "This is for three simple but structural reasons. First, equity markets have a tendency to go up, and ad valorum fees give fund managers leverage to this tendency and protect margins when costs are rising; secondly, technology change will lead to significant cost savings for managers; thirdly, economies of scale are meaningful and we are hoping to invest only in fund management winners that can use increasing scale to offset fee pressures."

In addition, he continues, each of the three shares look attractively priced on one of his favourite valuation measures – the AUM/EV ratio, which divides a firm's assets under management by its enterprise value.

Buying the cream of the crop

As a whole Train's portfolio would be regarded by some as 'defensive', while some of the stocks he invests in have been dubbed expensive 'bond proxies'. But he looks at it differently. "For me there are only two types of investor: momentum or value. I am not a momentum investor, so by definition I can only be a value investor.

I think Diageo (which some call a bond proxy) is cheap, but the reason why I think it is cheap is because it offers investors exceptional predictability, as in decades to come I expect consumers still to be consuming their products."

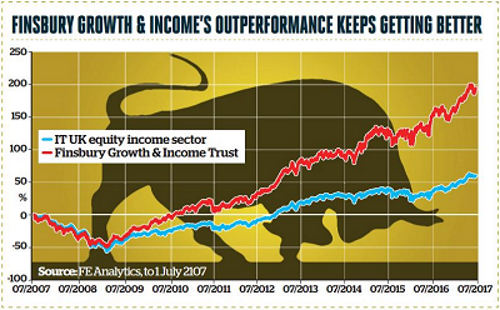

Train is a manager who cannot be accused of being an "index-hugger", nor can even the most ardent passive fund enthusiast make a case that he is simply lucky. Over various timeframes, short and long, he is ahead of both the competition and the wider market. On a 10-year view, as the chart opposite shows, FGT is up 195%, while in contrast the average UK equity income trust has produced gains of 60%.

Moreover, the trust is streets ahead of the FTSE All-Share index's 72% rise. In contrast to passive funds, Train's portfolios hold only what he perceives to be the cream of the crop. It is a winning formula.

Train in Six

1. My best investment was.... , over 20 years ago, when it had a dozen or so regional independent television companies. In the process, I learnt a valuable lesson – don't underestimate a business that can capture people's attention.

2. My worst investment and lesson learnt.... the most painful one that sticks in my mind was when I predicted the US economy would go into recession. It was at some point in the 1980s, and because I felt so sure it would happen I made the portfolios I was running more defensive. My prediction was correct, but what I got completely wrong was how the stockmarket would behave – it went through the roof. I learnt that the stockmarket and the economy are two completely different things.

3. Alternative career would have been....I'm too much of a dilettante to have done anything else.

4. In spare time I like to....I enjoy practising yoga; I am a qualified yoga teacher.

5. The one thing I would like to see change financial services... for investing to be as common a thing as having a flutter on a horse race.

6. Do you invest in the trust... I do indeed, and actually don't personally invest in the open-ended version – CF Lindsell Train UK Equity. I prefer investment trusts anyway, but I also wanted to align my interests with FGT shareholders when we launched the open ended fund in 2006. I wanted shareholders to know that I remained fully committed to the investment trust.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.