Why this panel of experts is still cool on UK shares

6th November 2017 09:53

by Jim Levi from interactive investor

Share on

Donald Trump's promise to "Make America Great Again" could mean a weaker dollar. The US president's protectionist instincts make him want to boost American exports and inhibit foreign imports.

In addition, he likes low interest rates, as these - combined with proposed hefty cuts in income and corporate taxes, and his plans to deregulate the banks to encourage more lending - comprise the policy blend he has chosen to revive the jobs market in places like Ohio and Pennsylvania that proved crucial to his poll victory last year.

The hope is that Trumponomics will turn the US's unremarkable growth rate of 2% to something nearer 3% in 2018, and thereby prolong the US recovery.

The current period of expansion is already the third-longest in US history, and if Trump manages to keep the momentum going for another 18 months it will break all records.

This prospect has already sent equities on Wall Street to all-time highs this autumn.

In recent months the fashion has been to switch investment funds out of the US and into Europe, where growth has resumed and good value in equities is easier to find.

According to a Merrill Lynch survey, interest in eurozone shares is at a 10-year peak among wealth managers. But Wall Street's recent impressive momentum is prompting some rethinking about US equities among our panel of asset allocators.

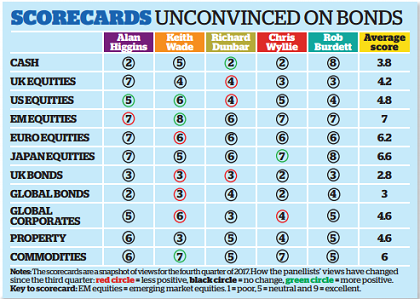

Significantly, the average score on the US equities sector has crept up from 4.4 to 4.8. Schroders' Keith Wade (up from 4 to 6) and Coutts' Alan Higgins (up from 4 to 5) have both increased exposure.

"The recent trend has been to switch funds out of the US, where value is hard to find, and into Europe," Wade says.

"But I prefer to be more neutral between the two. I quite like both markets now." Higgins points out: "There are stocks you can buy in the US that you cannot very easily obtain in other countries' stockmarkets, in areas like biotechnology."

"Maybe we are back in the old game of playing currency wars," comments Connor Broadley's Chris Wyllie.

"Growth shifts from one region to another, depending on who has the weaker currency." But he warns that the mood could change quickly at a time when currencies are volatile. "When any pick-up in US growth starts to become noticeable, the dollar might then recover."

Wyllie keeps his score at 5 for the US; but having moved some funds out of the US into European equities in June, he is now putting some money back into Wall Street, as he sees opportunities for sector rotation into lower-rated banks and energy stocks.

Higgins points up the contrast between high-tech US stocks such as electric car-maker , which is selling on more than 70 times the hoped-for earnings in 2018, and the old technology car manufacturer , yielding 5% and selling on just six times expected earnings. "Some people are saying the big car giants have six or seven years left and then they are obsolete," he says.

Opportunity to take profits

However, Standard Life Aberdeen's Richard Dunbar sees the recent firmness of US equities as an opportunity to take some profits. He has lowered his score a notch from 5 to 4, while raising his score for cash from 1 to 2.

Meanwhile, F&C's Rob Burdett remains sceptical about the credibility of the current US administration: "There has been a huge staff turnover at the White House but not a lot done." He stays underweight at 4.

As the year draws to a close, Higgins concludes that 2017 is proving to be "quite a special year, because we have synchronised economic growth around the globe. That does not happen very often and I think financial markets have been a little surprised by it."

The widening of the global recovery has led to better-than-expected results across a broad spectrum of companies and markets. Wyllie thinks corporate earnings forecasts "will be higher at the end of this year than they were at the beginning, when the economic recovery appeared to be petering out. That is very unusual. It is usually the other way about."

Certainly, the correction in the long bull run in equities so widely predicted has not happened yet.

In nearly all major markets the summer has been characterised by a broadly sideways movement.

The exception has been the US market, but even here Wall Street has not performed that well for UK investors after adjusting for the fall in the dollar against the pound.

As Wyllie points out: "Corrections can occur in stockmarkets in a number of different ways, and one of them is the sort of sideways movement we have been having during the summer."

If the dollar is weaker, the other side of the coin has been the end of the Brexit-triggered run on the pound. From a low of under $1.20 in January, sterling has slowly clawed its way back to a recent year high of $1.36. (Nonetheless, it's hard to believe that less than four years ago it was trading at $1.70.)

Since the spring Higgins has been predicting a recovery in the pound, and he thinks this may continue. "We think sterling should be back over $1.50," he says. Wade of Schroders is also quite supportive of the idea that the dollar could weaken further against the pound in the weeks ahead.

US interest rates to rise

He points to the continued very low inflation levels in the US. "That has led to a reappraisal of the policy on interest rates by Janet Yellen and her colleagues at the US Federal Reserve," he claims.

"Among economists the consensus is for an interest rate rise in December, but we think there will not be a rate rise until June of next year. Indeed there may be only one US rate rise in the whole of 2018."

Despite the positive fundamentals, however, a lot of gloomy thinking prevails. As a consequence, when it came to marking the 10th anniversary of the banking crisis and the collapse of Lehman Brothers and Northern Rock, most commentators were fretting about when the next crisis was coming.

As Wyllie says: "People seem slow to realise we are in a benign environment. They are counting down the days to the next problem. It is a "glass half empty" view of the world, rather than one where the glass is filling up." He points to what he describes as "the extraordinary appetite" investors still have for low-yielding long-dated government bonds. "They must still believe there is no growth recovery going on," he says.

Our panel have mostly resisted this widespread pessimism, and continue to favour equities over government bonds.

Higgins gives a score of just 2 for global government bonds, because of the currency risk for UK investors if the pound continues to recover. Apart from Wade and Burdett of F&C Investments, the panel's cash levels remain low. And even Wade has generally increased his exposure to equities.

Unloved UK market

However, the clouds do hang over UK equities as the nation faces the twin uncertainties of Brexit and the lurking shadow of Labour chancellor-in-waiting John McDonnell's anti-capitalist views.

"The UK is a very unloved market," warns Higgins. But to any contrarian investor such words could sound very sweet indeed. Certainly Higgins himself continues to bet against the crowd, giving UK equities a score of 7.

The rest of the panel are all underweight, although Burdett (current score only 3) admits: "I may want to raise that score soon, but not yet."

In the bear corner, Wade continues to make negative noises: "The potential ending of the cap on public sector pay might lift the pound further as the Bank of England is prompted to raise interest rates; leading UK shares are heavily driven by sterling and a strong pound might be a stumbling block for our overseas earners. Meanwhile, the underlying economy is showing signs of slowly decelerating."

Our panel remain overweight in both Japanese and European equities, although Wade has also lowered his score for Europe from 7 to 6. "I think the strength of the euro may bite into corporate earnings projections," he says.

Wade is more cautious than the rest on Japan too, with a score of only 5. "We still like Japan, but we are concerned about the strength of the yen and about the effects of the North Korean crisis on the region."

Burdett, in contrast, focuses on corporate performance. "Results are coming through really well and the local fund managers we talk to remain very positive," he says. His score remains 8.

Emerging market equities remain the panel's favourite sector, and the average score is now 7.

It is not hard to see why. The broadening-out of economic recovery, a better than expected performance from China, the weakness of the dollar and the strengthening of commodity prices are all favouring the sector.

"Emerging markets still look cheap despite the outperformance over the past 18 months, mainly because earnings are coming through at a greater pace," says Burdett.

Wyllie thinks Latin America could be the next area of emerging markets to catch up with markets in Asia. Wade, meanwhile, likes emerging market sovereign debt.

"If we could score that sector, we would give it a 6 or a 7," he says. That compares starkly with the 3 he scores for the global bonds of developed economies.

Two contrasting views emerge on global corporate bonds. Wade shaves his score from 7 to 6, but still think they are an appropriate diversifier in a relatively benign economic climate.

But Dunbar, on a score of 3, believes that "we are not paid enough for taking the extra risk". The yield attractions of property shares remain, but enthusiasm is muted. All panel scores for the sector are unchanged.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.