G4S finds support after early dive

7th November 2017 13:00

by Graeme Evans from interactive investor

Share on

warning about continued tough trading in the Middle East and India shouldn't have come as much of a surprise to investors today. Oil prices have struggled until recently, while chief executive Ashley Almanza pinpointed the region in the summer as one area of "elevated uncertainty".

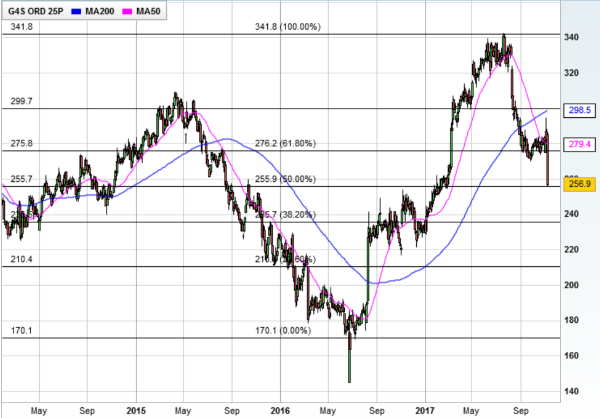

Unfortunately for G4S, the City is in no mood to forgive slip-ups in the outsourcing and support services sector at the moment. Shares were duly punished, with the recently promoted FTSE 100 stock off over 8% to 255.8p, an eight-month low.

The slump leaves G4S in danger of losing all the share price gains racked up during an impressive first half of the year. Caution is now the watchword, particularly after recent disappointments in the outsourcing industry.

Only last week, Jefferies and Deutsche Bank upgraded their ratings to 'buy', with targets of 330p, arguing that the recent fall in price appeared overdone. In early August, before G4S's last warning, the shares were being bought for 336p.

G4S, which employs more than 580,000 people involved in security guarding, running prisons and transporting inmates, and collecting cash from high street stores, said today that revenues were expected to grow by 3% to 4% this year. That compares with guidance earlier this year for an improvement of 4% to 6%.

Excluding the Middle East and India, G4S pointed out that growth had been 6.1% in the first nine months of 2017. The quality of the group's bid pipeline and contract win momentum remains encouraging, it added.

The company is also buoyed by the way its secure solutions business is making inroads into the field of systems and technology enabled security, accounting for over £1.7 billion in annualised revenues.

The downside, however, continues to be provided by the Middle East, where revenues fell 7.8% and profits were down 24% in the first six months of the year.

In the summer, Almanza told analysts: "For some time now we've been highlighting the risk to the downside in the Middle East, India region, not least because of the prolonged period of low oil and gas prices."

"We're cautious about the prospects in the near term in the Middle East and in the UK because in both of those markets there's elevated uncertainty."

All of the regions apart from the Middle East grew in the first six months of the year. Africa saw a continuing recovery with 6% revenue growth, with more modest performances in Asia Pacific and Latin America.

North America has now overtaken UK & Ireland as G4S's biggest market, driven by demand for its cash management services and as the company reduces its dependency on its home market after a series of blunders.

At 257p, G4S shares trade on 12.8 times the 20p of earnings per share pencilled in by UBS for 2018, and offer a prospective dividend yield of 3.6%. That profits multiple is a discount to the sector and does not look stretched.

There's solid technical support at around 255p, too – the 50% retracement of the rally from summer 2016 levels (ex-Brexit) to July 2017 high. However, investors will demand evidence of improvement in the Middle East before chasing the shares beyond resistance at 275-285p.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.