The risks and rewards of investing in Latin America

11th April 2018 10:44

by Tom Bailey from interactive investor

Share on

When investing in emerging markets is spoken of, most people's minds wander to Asia. Whether it's excitement over Chinese technology companies, hope that India will be the new China, or a wish to get in from the ground up in frontier economies such as Vietnam, Asia is the focus of most investors' attention in 2018 (as it was last year).

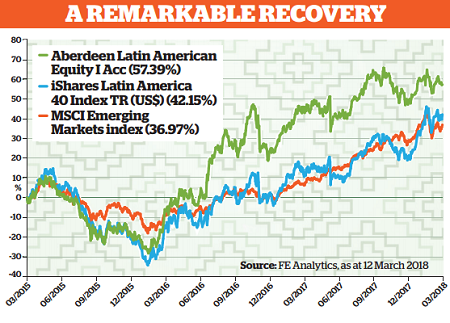

However, when you look at passive returns from the first three months of 2018, Asia's emerging and frontier economies have been eclipsed by returns from Latin America, which have surged ahead. has produced a three-month return of 16.8% to 8 March. In comparison, the wider 's three-month return was 8.9%, while iShares MSCI All Country Asia ex Japan ETF produced 5.9%.

Of course, index returns are not the be-all and end-all, but it is notable that Latin America's index has outperformed both the broad emerging market and Asian indices. As the US magazine Barron's summed it up in February: "A weird thing happened in emerging market stocks after this month's market stumble: Latin America started outperforming."

Source: FE Analytics Past performance is not a guide to future performance

Return to growth

This strong performance, says Chetan Sehgal, the recently appointed lead portfolio manager of , "was driven by a supportive global environment, higher commodity prices and stronger regional currencies." Against that backdrop, over the past year Latin American economies have seen significant improvement.

"Latin America saw an extended period of underperformance from 2011 through to 2016, resulting from challenging global conditions as well as domestic factors," says Tom Smith, head of Latin American equities at Neptune. Since then, however, "the investment case has transformed dramatically, with much more supportive global conditions and a significant improvement in the political landscape across the region."

Last year, the region saw a pick-up in economic performance, with annual growth of 1.9% in 2017 - one of the strongest readings in recent years. And this uptick seems set to continue. "There is an expectation that most countries will be posting better growth this year than last," says Will Landers, manager of the .

Smith adds that the two countries leading the pack are Brazil and Argentina, both of which emerged from recession in 2017. However, other countries such as Peru and Chile have also seen relatively strong growth.

Brazil has a huge influence on the overall region and comprises 60% of the MSCI Emerging Market Latin America index. The country's recovery has come following a difficult period. Having been feted as one of the emerging BRIC economies in the 2000s, its economic fortunes started to decline in the 2010s. "Particularly during 2015 and 2016, Brazil was mired in its deepest recession for decades", notes Smith.

Now, however, it is "clearly in economic recovery mode," according to Landers. Successful attempts to bring inflation down allowed Brazil's central bank to start cutting interest rates in 2017 - a good move for economic growth. And the bank still has room to reduce rates again this year. The economy is expected to grow by around 3% this year.

Moreover, Brazil's recent success is not as dependent upon commodity exports (which account for around 5% of GDP) as in previous bouts of growth. The current economic upswing is coming from across the economy, from industrial production to retail sales, says Landers. Brazil's middle class is continuing to grow, and the consumer side of the Brazilian economy "is definitely in recovery."

As Sehgal notes, "Brazil, as the largest economy in the region, has a large consumer market, which will be an important driver of growth during the ongoing economic recovery." Profits among Brazilian firms are also looking healthy, owing to their low levels of debt.

All of this makes Brazil once again an attractive prospect for investors. "No one wants exposure to Latin America unless Brazil is in there," says Landers. His own fund has 68% in the region.

Argentina's growth is expected to be even stronger than Brazil's, at 3.5% this year. It is currently undergoing a process of normalisation that should lead to it being upgraded from frontier to emerging market status this year. As Smith notes: "In 2016 Argentina underwent a painful adjustment as president Mauricio Macri implemented structural reforms in an effort to address the imbalances after over a decade of Kirchner rule."

Smith is also positive about other, less prominent economies in the region. "Meaningful acceleration is also expected in Peru and Chile, with Peru recovering from natural disasters early in 2017 and Chile seeing a marked pick-up in consumer and business confidence following the election of Sebastian Pinera in December."

Political upset on the horizon?

For investors, politics is always one of the key risks surrounding the region. While the decline in commodity prices in the early 2010s hit Latin American economies hard, domestic policies exacerbated the region's woes. As noted above, the turnaround for the region came with the ascent to power of more pro-business politicians. As Smith observes: "After shifting to the left from the early 2000s through to 2015, more recently we have seen successive elections won by market-friendly and pro-business presidents."

However, with many Latin American countries hosting elections this year - most importantly Mexico and Brazil - the question is whether this trend will hold. "Brazil's near-term outlook is challenging in light of the 2018 presidential elections, which could bring higher volatility," says Sehgal. The biggest concern for business right now is the return to power of former president Luiz Inácio Lula da Silva, known as Lula, in the country's October election.

As leader of the Workers Party, Lula is expected to put a stop to many of the current reforms being carried out. At present, he leads in the polls. However, owing to a corruption conviction, Lula may be barred from the race. "There is likely to be a lot of noise around Lula," says Landers, "but he won't be able to win."

Arguably more of a risk is the election of the left-wing populist Andrés Manuel López Obrador, known as AMLO, in Mexico's October poll. Right now, he is leading in the polls.

Another potential upset for Mexico centres on the ongoing North American Free Trade Agreement (Nafta) negotiations. US president Donald Trump wants to renegotiate the trade pact - to the benefit of the US. "The Mexican peso and the Mexican stockmarket have been very weak following the election of Donald Trump," says Smith.

However, he continues: "Round seven of talks is ongoing in Mexico City and the tone of comments is getting increasingly constructive." While there will likely be volatility as a result of both Nafta negotiations and the elections, Smith thinks there are still "a number of excellent opportunities in Mexico", from which investors can benefit.

Landers cautions that the uncertainty over the potential for AMLO coming to power and Nafta negations is likely to result in Mexico's economic growth remaining flatter this year.

How to invest in Latin America

As is always the case, getting exposure to the region through a passive fund is the cheaper option. This is particularly so for Latin America, where active management fees can often be higher than for other regions. According to a recent report by Canaccord Genuity, active Latin America funds typically cost between 1.2 and 2 %. By contrast, ETFs cost between 0.6 and 0.8%.

Index trackers in the region, however, are more likely to expose investors to a few very specific sectors that dominate the economy - chiefly financials, energy and mining. For instance, iShares Latin America 40 ETF has a 10% weighting to the large Brazilian bank Itaú Unibanco. Other financials also dominate the index's top holdings, as do huge Mexican and Brazilian oil producers.

Having a high exposure to these sectors isn't necessarily bad in the current economic climate. Oil is seemingly still in recovery, while a growing economy is supportive of financials; but these sectors are highly cyclical. Investors looking for greater exposure to the region's growing consumer economy and steadier growth may wish to look to active managers. Moreover, there are still a lot of market inefficiencies, potentially giving active managers an edge.

This year, our sister website Money Observer added to its Rated Funds list. The fund has a strong emphasis on growing companies and is known for its intensive research and cautious approach, which lends itself well to investing in this relatively risky region. However, even so, its FE Risk score (which measures volatility in excess of that of the , rated at 100) is currently at 206, which is pretty high.

Ben Yearsley, director of Shore Financial Planning, recommends a different, less risky route to exposure, through broader emerging market funds that are overweight on the region. "I'm less keen on pure Latin America exposure and have tended to largely avoid it," he says.

He likes , which has 12% of its holdings in Brazil, as well as , with 13% in Latin America. He also notes that "tends to have more in Latin America than many of its peers," with 15% currently in Brazil, as well as exposure to Argentina and Peru.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.