Jargon buster: Does Mifid II matter to you?

20th April 2018 10:04

by David Prosser from interactive investor

Share on

It has been seven years in the making and runs to 1.4 million paragraphs, but will the European Union's new Markets in Financial Instruments Directive (Mifid II) have any impact on private investors? Potentially, says the asset management and stockbroking industry - and investors will be wise to treat the regulations with some caution.

In fact, Mifid II is already here, having come into force on 1 January 2018. Many investors will already have been affected - the directive requires financial services businesses to maintain more detailed records of clients, prompting many firms to write last year to investors requesting updated personal information.

If you received such a request, it was likely to be Mifid II-related - and if you ignored it, you may find yourself unable to trade on fund platforms or through intermediaries until you've provided the details required.

In the months and years ahead, however, regulators' ambitions for the directive are more wide ranging.

They hope it will improve competition amongst investment services providers while enhancing consumer protection, with the first version of Mifid, introduced in 2004, widely regarded as having forced down prices and improved transparency.

The most visible area of change concerns fund charges, with asset managers now required to provide more detail of the costs to investors of holding their funds.

In addition to the ongoing charges fee (OCF) that managers are currently required to disclose to investors, they will also have to publish the transaction costs that the fund incurs when buying and selling portfolio holdings.

This is important, argues Philippa Gee, the managing director of Philippa Gee Wealth Management, as many investors don't realise how significant these charges can be.

"Investors will find they have more information about charges, both those deducted to date and those going forward," she says. "This should make it easier to compare and contrast investments, helping the decision-making process."

Some analysts expect greater fee transparency to have profound effects, challenging commonly held assumptions about the cost of investments.

For example, funds investing in illiquid asset classes, where transaction costs tend to be much higher, currently appear to be cheaper than they really are.

Similarly, index-tracking funds, routinely sold to investors as low-cost options, also tend to have relatively high transaction fees as they must trade regularly to track the market accurately.

Even plain-vanilla funds rack up surprisingly high transaction costs. Analysis published by the consultancy Fitz Partners suggests the OCF of the average equity fund would increase by 21% if trading costs were added.

That figure rises to 26% and 29% respectively for index trackers and exchange traded funds.

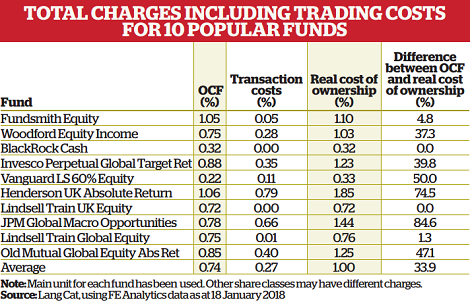

For some funds, the before- and after-transaction costs comparison is even more striking. Analysis from the Lang Cat consultancy reveals, for example, that 's true charge rises to 1.85% once you add transaction costs of 0.79% to its stated OCF of 1.06%.

At low-cost tracker , the 0.22% OCF rises by half as much again once you add in transaction costs of 0.11%.

The point about these fees is that investors have always paid them - just without realising it until now. Mike Barrett, a director of the Lang Cat, describes the issue of transaction costs as 'a bit grubby'.

"From an investor's point of view, it's likely to be a real turn-off," Barrett says. "People regard financial services at roughly the levels of trust normally reserved for politicians and estate agents; with fund groups now saying, "oh, sorry, when we said we were charging you x, we actually meant a figure over a third higher", it's not hard to understand why."

Low cost and good value

In that sense, Mifid II is doing investors a good turn, forcing managers to provide a much more honest account of the costs their customers have been incurring for years.

The counter argument, however, is that low cost doesn't necessarily equal good value: where funds are incurring higher transaction costs from trading that delivers superior performance, many investors will be happy to put up with these charges.

Some in the asset management industry fear that a single-minded focus on charging will commoditise their business, inhibiting innovation and limiting choice.

It's also fair to point out that consistency is an issue. Ian Sayers, the director general of the Association of Investment Companies (AIC), warns that the patchwork quilt of regulation which now applies could mislead investors.

One problem is that Mifid II only applies to investment products, so comparisons with other types of retail savings product will be confusing.

Source: Lang Cat

Another is that the new regulation came in at the same time as the European Union's Packaged Retail and Insurance-based Investment Products (Priips) directive, which imposes an additional raft of disclosure requirements; to add insult to injury, Priips currently only applies to certain funds - notably the investment companies that make up the AIC's membership, but not most open-ended vehicles.

"The issue is not whether people should or shouldn't have access to this information, but that they should be able to compare like with like," argues Sayers.

"In fact, history shows that if you provide people with too much information or data that is too granular, they tend not to read it or to understand where the inconsistencies lie."

Some advisers fear this increased frequency of reporting may also encourage investors to become more short-termist.

In the corporate world, an ongoing backlash against quarterly reporting by companies is based on exactly this fear - that it encourages investors to focus on the here and now rather than the long-term performance they're really seeking.

Retail investors must avoid falling into this trap, chopping and changing portfolios too often, racking up costs in the process.

A particular disclosure worry for many advisers is a new Mifid II requirement concerning clients whose portfolios they manage on a discretionary basis, rather than offering advice or providing execution-only services.

Where such clients' portfolios suffer a drop of 10% or more during a three-month period, advisers and wealth managers will now have a statutory duty to point this out to them.

"It's questionable whether telling an investor that his or her portfolio has fallen by 10% is a smart move; investments are by their nature volatile and volatility is a price that investors pay for potential reward," argues Martin Bamford, the managing director of independent financial adviser Informed Choice.

"Worrying investors by telling them when that volatility has occurred could prompt some negative behavioural outcomes, such as selling when markets have fallen."

Lower-risk asset classes

Ian Sayers is also concerned by this possibility. "Does this start encouraging investors to move towards lower-risk asset classes?" he asks.

"It's a good example of the conversation that regulation often forces us to have about risk -it completely misses the discussion about the danger of not achieving your long-term financial goals because you're in low-volatility asset classes."

That potential counter-productivity is mirrored in another area where Mifid II has implications for retail investors.

As with transaction costs, the regulation also requires money managers to split out and publish the costs of investment research, which have until now been bundled in with trading fees.

The effect is likely to be particularly pronounced in areas where research is more specialist and therefore less easy to access. At Livingbridge Equity Funds, fund manager Ken Wotton says smaller companies research is a particular concern.

"With less pre-packaged insight and research available going forward, investors considering smaller quoted companies [funds] need to consider how best to access potential returns from growth companies, whilst mitigating the associated risks," he argues.

Still, the jury is out on this one, with many fund managers arguing that there is little evidence as yet of any decrease in the amount of research available, even in niche areas. Indeed, some managers may seek to add value by adding to investment in research rather than cutting back.

Nevertheless, this is another area investors will need to keep an eye on as Mifid II continues to bed in over the next 12 months. As ever, the law of unintended consequences remains powerful.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.