Fund manager view: An AIM gem, Brexit and risk

11th May 2018 11:43

by Marina Gerner from interactive investor

Share on

Many eyes turned to boutique fund manager Sanford DeLand at the end of 2016, when one of the UK's most successful fund managers, Rosemary Banyard, joined its small team as investment director.

For 18 years she was known for running the with Andy Brough, as well as heading up several other UK smaller - and mid-cap funds, managing assets totalling around £1 billion.

At Sanford DeLand she launched and now manages the £10 million , which launched at the start of 2017.

It invests in UK companies across the market-capitalisation spectrum, including those listed on the Alternative Investment Market (AIM). She works with Keith Ashworth-Lord, who set up , aiming to mirror Warren Buffett's investment approach.

'I still want to run money'

Over lunch at an Italian restaurant, Banyard tells me that after leaving Schroders, she "thought about pursuing something very different, maybe non-executive directorships". But she soon realised that she "still wanted to run money" – her first love.

he considered starting her own firm, but Ashworth-Lord convinced her to join Sanford DeLand instead. She says: "It was a better option than setting something up from scratch, which would have taken time to get regulatory approval."

At Sanford DeLand she was given a blank slate for the Free Spirit fund. She chose a benchmark of inflation plus 2 % - "as an absolute minimum" - because she didn't want to be limited by the weightings in any given index. "Ultimately, it's our job to protect and enhance people's wealth in real terms," she says.

Banyard adds: "It's important to have people to bounce ideas off, who will spot something you haven't noticed that will enhance your portfolio. I had a very good working relationship with Andy at Schroders, and I was looking for another "partner in crime", though that's probably not the right phrase." When she met Ashworth-Lord it was "a meeting of minds".

So what are the differences between working at a big fund management group and her life now? For a start, she says: "I no longer commute to London (from Cambridge)." More significantly, her role is very different now. She explains: "I'm more involved in business decisions, not just with the Free Spirit fund, but with everything. I sit on the board and I have a shareholding in the business." She adds: "It's exciting to put my energy into a small business and try to add value, as there is plenty of scope."

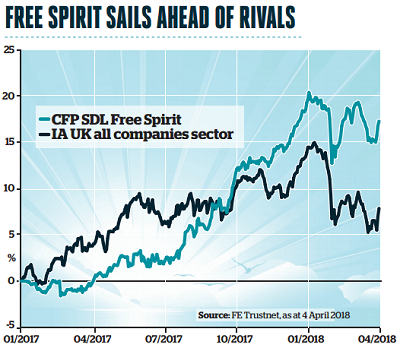

Source: FE Trustnet Past performance is not a guide to future performance

Previously, she had a dozen mandates of different sizes with different benchmarks. Now she runs just one fund.

It targets between 25 and 40 holdings, and currently has 33. Banyard keeps a watchlist of further potentially interesting companies. In comparison, she previously had about 200 investments to monitor. "Now it's simpler and more focused," she says. "I have time to model every company I own."

She credits Ashworth-Lord for her new rigour in modelling how firms are performing. The fund looks at every company's history over the past 10 years, analyses various ratios and then produces a three-year forecast based on each business's cash flow.

Of course, her previous working environment also had attractions; she says one of the benefits of her being part of a bigger fund management house, for example, was that she was a member of an international small-cap team. She found US and European smaller companies to be typically somewhat correlated to UK smaller companies, while Japanese smaller companies were not.

It is often said that a smaller fund can be nimbler in the way it invests. One crucial difference, Banyard points out, is that a larger fund has to invest in companies with larger market capitalisation.

If for example, you run a £300 million fund and you only want 30 holdings in your portfolio, with a smaller company mandate you would end up with a very large stake in any business you invested in. And that's risky.

You are also likely to find it difficult to buy sufficient shares. So inevitably, you have to either increase the number of holdings in the fund or move up the market-cap scale.

That means your companies are likely to be better covered by other analysts, so your chances of finding an 'undiscovered gem' flying under the radar are reduced.

One such company is . Banyard holds this AIM-listed company, which is one of just a few businesses worldwide that specialise in infection prevention in human and animal healthcare and contamination control - producing niche products to help disinfect outpatient medical equipment in hospitals, for example. "If you want those kinds of firms, you can't have them in a big fund," she says.

However, she emphasises that the business proposition has to be something simple enough to be explained to others. "I have found over the years that you shouldn't invest in something you can't explain."

Banyard favours businesses with what Warren Buffett famously described as 'moats' -barriers to entry against competition that protect their long-term profits and market share. "Lots of companies tell you that they have one. But it's easy to see if they have high profit margins and above-average returns on equity without having too much debt. Their profits need to be backed up by cash flows."

She says such characteristics tell her a company must be doing something right, but that "you have to pick through a lot' to find a company that meets these criteria. She adds that the average return on equity of a UK company after tax is 13%, but that she is "looking for something better than that".

Opportunity springs from volatility

stockmarkets have been volatile recently. So what might be the risks on the horizon? Banyard says she generally sees the kind of market volatility seen in recent months "as an opportunity to top up holdings that may have suddenly dropped in value for the wrong reasons".

She emphases that it's crucial to "not be panicked by panic". She says: "[A company] has an underlying value and the share price wings around that, so I'm trying to find times when it's below it".

She mentions how when she first joined Schroders she used to observe the highly regarded fund manager Jim Cox. Instead of frequently buying and selling stocks, he spent a lot of time just looking at his screen "and on a bad [market] day adding to his existing holdings."

When it comes to Brexit, she remains reasonably relaxed: "If a company is fulfilling a need, I shouldn't worry about what Brexit will look like." She adds that diversification should help protect her portfolio from external political risks. The fund currently has 16% of its holdings in software companies, 13% in financial services and 6% in each of the travel, leisure and media sectors.

We turn to the role of women in finance. Only 8.5% of fund managers are women, according to research by Tilney Bestinvest from 2017. Yet studies have shown that female hedge fund managers tend to outperform their male counterparts. One possible explanation for this is that in order to succeed in a male-dominated industry, women who end up as fund managers tend to be the cream of the crop.

I ask Banyard what she makes of the lack of female fund managers in the industry. "I wish there were more," she replies.

However, she observes: "There is still a bit of a culture that standing up and making a lot of noise attracts attention in the retail world."

One might add that Banyard's performance speaks for itself. In its first year her Free Spirit fund returned 18.5%, while the Schroder UK Mid Cap trust returned 16 % a year while she was in charge (May 2003 to September 2015).

Banyard says there needs to be more awareness at school and university level that "women have found that working in fund management works well with having a family", as she herself has. However, she adds: "For it to work best, it's good to have joint responsibility". That rings true both for women's private and for their professional lives.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.