China funds present opportunity after Trump trade threat

16th May 2018 09:04

by Cherry Reynard from interactive investor

Share on

It was all going so well. Chinese markets had a barnstorming year in 2017; the consumer-based economy flourished and technological innovation forged ahead. But US president Donald Trump is now threatening to put a stop to all that. Tariffs have been imposed, knocking markets lower and threatening to disrupt the momentum of Chinese economic expansion and stockmarket growth.

In mid-March, on his mission to "make America great", Trump announced $60 billion (£48 billion) of tariffs on Chinese imports. For good measure, he said China needs to pay a price for unfairly acquiring US intellectual property. China's initial response seemed moderate in comparison: retaliatory tariffs of just $3 billion. These applied to US steel pipes, fresh fruit and wine, pork and recycled aluminium.

- Trump's olive branch and new Italy crisis

- Two great investments in the world's best consumer story

- 10 most popular funds - April 2018

Markets rattled

While all global stockmarkets responded badly to news of the US tariffs, Chinese markets were particularly hard-hit. China is the clear focus of Trump's ire and, in spite of the country's moderate early response, it is difficult to see how this can end well. Nevertheless, trade wars are likely to raise the cost of consumer goods for US citizens, which may prove too high a political price for Trump and curb his enthusiasm.

May Ling Wee, investment manager of the , says that while a lot of the Chinese market is exposed to the domestic rather than the global economy, there are still risks: "If global trade deteriorates, it detracts from Chinese GDP. It also hurts sentiment, and that is where the impact is being felt today. Some companies have been sold off indiscriminately."

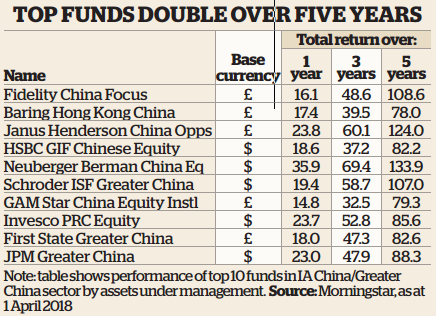

Up to this point, it had been boom time for Chinese stockmarkets. The average China/Greater China fund was up 23% over the 12 months to 23 March, according to data-provider FE, putting the sector top of the Investment Association sector league table. Those who had the foresight to be invested five years ago would have made an average 87%.

Source: Morningstar Past performance is not a guide to future performance

Technological muscle

That said, there is almost 60 % between the top - and bottom-performing funds – GAM MultiStock China Evolution Equity at the top and at the bottom. This is a reflection of the relative concentration of market performance in just a few stocks. In this way, Chinese markets have mirrored those in the US, where the large technology names have dominated. China's very own FANG equivalents - notably and - have hauled markets higher.

Gavin Haynes, investment director at Whitechurch Securities, says: "This has been a phenomenal period of performance and a key driver of stockmarket performance in the wider region. However, performance has been driven by the technology sector, where there were a number of exceptional stockmarket performers. It is symbolic of the shift in the Chinese economy from manufacturing to domestic consumption; Alibaba and Tencent are becoming household names."

As a result, funds focused on consumers and, particularly, consumer technology have done well. The , has 10% each in Alibaba and Tencent, alongside holdings in other major technology-focused names such as , and . Weaker funds have taken a more 'value' tilt by focusing on old-economy areas such as manufacturing, where firms are cheaper but growth has been less buoyant.

There has also been a contrast between the 'A' share (domestic) market and Chinese shares listed in Hong Kong. The 'A' share market has technically underperformed the Hong Kong market, although Wee says several domestically listed companies such as China International Travel have done very well. Alibaba is listed in the US, and Tencent in Hong Kong.

The future for the Chinese stockmarket is less clear, however. Haynes says: "China has been growing by in excess of 6.5%, and we are starting to see that slow down." At the same time, he adds, valuations are quite stretched after the recent run and have only fallen back by 2-3% in the wake of the issues over trade.

Moreover, the political situation is uncomfortable. The Chinese Communist Party recently removed the rule that limits Chinese presidents to two consecutive terms in office, to allow the country's current president, Xi Jinping, to rule indefinitely. For now this means the reform agenda that he has spearheaded will remain intact. However, over the long term absolutism does not tend to be sustainable.

The concentration of technology companies in the Chinese market is worrying. More than 40% of the MSCI China index is comprised of technology companies. Alibaba and Tencent account for more than 30% combined. China may not have the data privacy concerns that are emerging in developed countries, but that is still a lot of exposure to two highly rated companies.

Nevertheless, there may still be some scope for expansion in the technology sector. Both Alibaba and Tencent are looking at new areas of development, and they continue to be at the forefront of artificial intelligence. Tencent is growing very strongly in gaming, for example, and the group has only just started to monetise its popular WeChat brand, which has close to a billion users. There are outsized opportunities in China - in areas such as travel and leisure, for example - that are difficult to find elsewhere, because of the sheer size of China's population.

Buying opportunities

Haynes still believes in China over the long term, and he suggests that any market falls in response to the 'trade war' represent investment opportunities. For all-out exposure to the 'new China', he suggests the Fidelity Chinese Consumer fund, run by Raymond Ma. This buys into changing consumption patterns in China. He also likes the team at Hermes.

One final thought comes from Andrew Swan, head of Asian Equities at BlackRock. He says:

"In China it is clear that data privacy is less of an issue than it is in the West. The government would like to know everything that goes on, so it is sponsoring the data collection process. China has a huge population and strong digital infrastructure, so it can capture the large volumes of data that drive algorithms and AI. China is positioning to drive AI over the longer term.

"In developed markets, there is a growing backlash over the way data is collected and used by technology companies, particularly in areas such as travel and leisure, on privacy grounds. This will limit the amount of data companies can acquire. In China, however, the country's extraordinary pursuit of data could be a turning point for technology globally. China could leapfrog developed countries on a long-term view. Data is more abundant there than anywhere else."

China is stealing a march on the West in myriad ways. Now may look like an uncomfortable time to be investing there, but Chinese growth should survive short-term political setbacks. Any opportunity to reinvest at a lower price should be considered carefully.

Janus Henderson China Opportunities

The , launched in 1983, has been consistently at or near the top of performance tables in recent years. It is currently first-quartile over one, three and five years.

The fund, managed by Charlie Awdry (since 2008) and May Ling Wee (since 2015), invests across the Hong Kong and domestic China 'A' shares markets, as well as in some ADRs, which are non-US firms (in this case Chinese businesses) listed in the US.

The fund is firmly growth-focused. It looks for companies where earnings are likely to grow ahead of expectations, either because of positive industry dynamics or good management decisions. Awdry says the volatility of Chinese markets often allows them to "buy from pessimists and sell to optimists".

The bedrock of Chinese growth, he believes, is growing consumerism. Not only is the government trying to steer the economy away from manufacturing and towards consumerism, but China's integration in the global economy is giving them new products to buy. Reform, particularly financial reform, is another driver for Chinese growth and Chinese shares.

This is reflected in the current portfolio. Alibaba and Tencent are in the top 10, but the group takes a broad view of consumer stocks, including areas such as motor manufacturing. It also holds a number of Chinese banks, property and insurance groups. It is selective in financials, believing that consolidation has given some groups pricing power but that this is not universal.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.