Croda International back on track

7th November 2014 10:40

by Lee Wild from interactive investor

Share on

Things are looking up at . The major exporter of ingredients for make-up, anti-wrinkle creams and industrial lubricants, has been hammered by the strong pound, but sterling has weakened against the dollar, at least, and underlying growth is picking up, too.

Sales accelerated at both the company's core divisions during the third quarter, driving sales at constant currency up 4%. Business at Croda's new and protected products (NPP) unit also picked up.

At the high margin consumer care operation, sales jumped by 4.2%, far better than the 1.6% improvement over the nine-month period. Personal care returned to underlying sales growth and crop care grew, too. First meaningful sales of pharmaceutical grade Omega-3 also helped. Meanwhile, at the performance technologies, sales were "very strong" across the board, up 8.2% compared with 5.7% for the nine months. Margins there rose by 150 basis points to 17.1%.

"This is encouraging, given challenging market conditions and the somewhat disappointing tenor of recent announcements," said James Tetley, an analyst at N+1 Singer.

Of course, foreign exchange issues remain. Currency moves wiped out £19.2 million of sales during the three months, which meant reported turnover fell 3.3% to £259 million. That, and £2 million of currency transaction costs, knocked £5.5 million off earnings, too, so operating profit dropped by 6% to £58.1 million. Pre-tax profit was flat at constant currency, but down 6% at £55.1 million including the FX hit. Both sales and profits at the much smaller industrial chemicals business also fell.

N+1 Singer View:

"The shares have recovered ground in recent weeks, influenced by press rumours of potential bids from the likes of Evonik, Solvay, DOW etc. We would not be surprised to see Croda ultimately fall victim to a larger global group but the timing of a takeover remains virtually impossible to predict. In the meantime we retain our 2450p target price and 'buy' recommendation, encouraged by today's update."

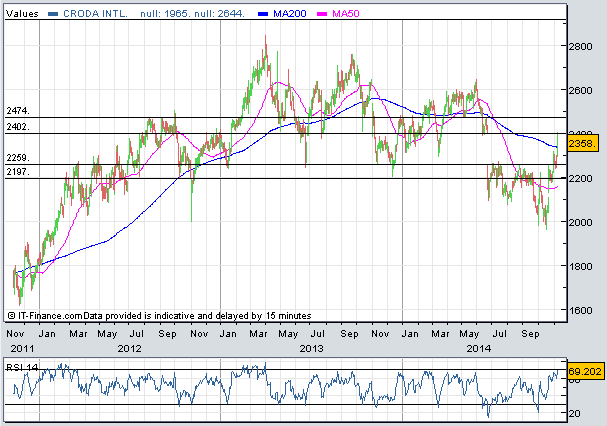

Croda has been the subject of takeover speculation for many years, so don't hold your breath. It may, however, underpin the share price. More important is the more rapid underlying growth, which Croda needs to justify high valuation multiples.

After rallying by 4% to 2,360p on these third-quarter numbers, the shares trade on 17.8 earnings estimates for 2015. The upcoming fourth quarter is, historically, the company's slowest, but Croda's superior margins deserve some credit, and hitting N+1 Singer's forecasts for growth in adjusted earnings per share of 6% for both 2015 and 2016 should be rewarded.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.