Where Lloyds could go wrong

5th August 2015 09:32

by Lee Wild from interactive investor

Share on

The reaction to second-quarter results has been largely positive. We reported how two brokers thought the shares would be worth 105p one day and predicted a prospective dividend yield of over 4% this year, rising to 6% and more from 2016.

But there are concerns in some quarters. French broker Exane BNP Paribas has just trimmed its 12-month price target by 5p to 90p to reflect cuts made to both earnings and dividends.

"The market reaction to 1Q15 results reflected increasing confidence that Lloyds was poised to deliver on the promise of becoming a major income distribution story," says Exane. "We still believe this to be the case but higher ongoing conduct costs and increasing competition in the UK mortgage market threaten to delay the full normalisation of dividend payments."

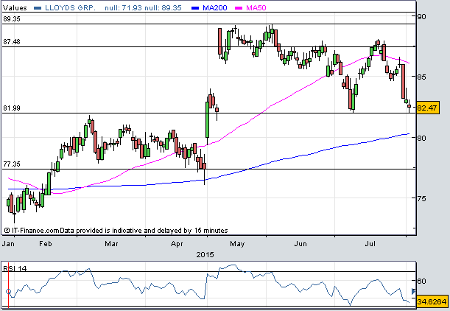

(click to enlarge)

Despite second-quarter net interest income (NIM) of 2.64% beating expectations, and full-year guidance raised from 2.55% to 2.6%, Exane has two concerns. Firstly, that guidance implies a softening in second-half margin, and secondly, it appears to require a moderation in volume growth to be achieved. The broker also trims net interest income forecasts due to a reduction in average interest earning assets.

And there's more. Lloyds' commitment to distributing all "excess" capital above a 12% CET1 ratio, plus one year's forward dividend payment, is broadly consistent with Exane's methodology. But it believes that uncertainty over issues such as risk-weighted asset (RWA) inflation and ongoing payment protection insurance (PPI) mis-selling costs "could delay Lloyds receiving the necessary regulatory approval it needs".

Exane has Lloyds paying a dividend of 2.75p this year, 4.5p in 2016 and 6.25p a year later. That implies a prospective yield of 3.3% in 2015, rising to 5.4% then 7.5%.

"We still view Lloyds as well placed given structurally higher returns and limited RWA growth, although it is important that margin trends do not start to disappoint," says the broker, which repeats its 'outperform' rating. "Lloyds should have enough liability repricing opportunities left to outweigh increased asset spread pressure but as other banks push hard in the mortgage space this becomes a source of potential disappointment."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.