Invest in trusts for a £10,000 income

5th February 2016 17:34

by Helen Pridham from interactive investor

Share on

Investment trusts are an attractive option if you are looking for ways to generate a regular income from your capital. They do not offer the monetary or income guarantees provided by cash deposits or annuities, but they do offer the potential of something better: a stable and growing income, inflation protection and capital appreciation over the long term - provided you are prepared to take some risk.

Most important, however, there is less risk of income fluctuations with investment trusts than with most other investments.

The advantage investment trusts have is that they can keep in reserve some of the dividends they receive from their investments each year. This money can be used by trusts to top up their own dividend payments if their investment income subsequently falls. This enables them to ensure their shareholders receive a reliable income even in leaner years.

For instance, as Ewan Lovett-Turner, investment trust specialist at Numis Securities, points out: "Most investment companies maintained dividend growth through the 2008/09 global financial crisis, at a time when many open-ended funds were forced to cut dividends."

Some trusts have enough in reserve to cover their dividends for a whole year, even if they receive no income from their own investments. Nowadays they can also dip into their capital to boost their income if they need to. Stability of income is important, but investors also need an increasing income if they are to be able to maintain their expenditure as prices rise.

Some trusts explicitly target an income rising in excess of inflation and have delivered on this promise. Indeed, some have been able to pay increasing dividends for nearly five decades. Although their share prices may have fluctuated over short periods, the overwhelming majority of equity-oriented trusts have also achieved capital growth over the long term too.

Putting together a portfolio

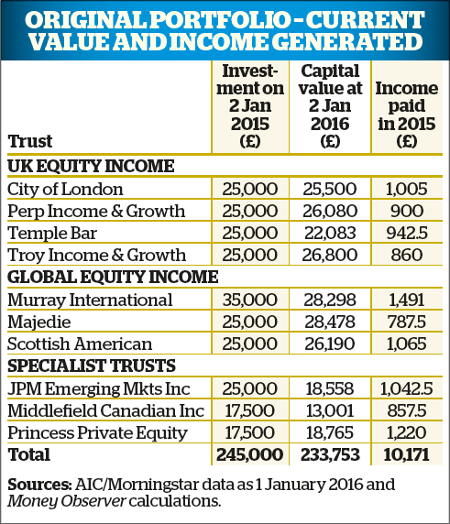

In order to demonstrate how trusts could be used to provide a meaningful income, in February 2015, our sister magazine Money Observer put together a portfolio of 10 trusts which, it was estimated, would pay a starting income of around £10,000 a year.

To achieve this income, it was calculated an initial investment of £245,000 would be required. The portfolio consisted of a mixture of mainstream UK-invested and global generalist trusts combined with some specialist, higher-yielding but potentially riskier trusts.

Overall, the original portfolio produced slightly more income in 2015 than we had estimated. However, the disappointing share price performances of some of its holdings led to a drop in its capital value of 4.6%.

In the next section we take a closer look at how the individual holdings performed, and the reasons for their progress - or lack of it. We also explain why we have decided to change two of the holdings.

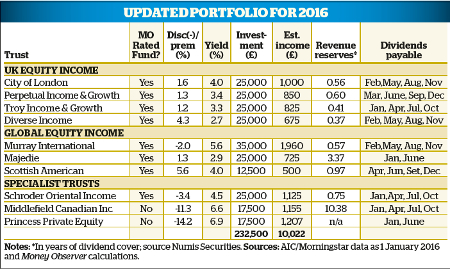

For any who are considering following this strategy, we give suggested investments in each of the trusts in order to achieve a £10,000 income. The good news is that somewhat less capital - £232,500 - is now required to achieve the same estimated income.

However, do remember that there are no guarantees that the portfolio will achieve its objectives; if you are in any doubt about whether it is appropriate for your needs, you should consult an independent fi nancial adviser.

UK exposure

At the foundation of the portfolio are four UK-focused income trusts, accounting for around 40% of the total. On the income front, none of our original holdings disappointed and three of the four trusts also produced varying amounts of capital growth.

continued its record-breaking run of continuous annual dividend increases last year, making 2015 its 49th year of unbroken growth. Its dividend was increased by 3.7% and revenue reserves were also raised for the third successive year.

The conservative approach taken by Job Curtis, its manager since 1991, continued to pay off. He focuses on companies with cash-generative businesses and attractive yields which are able to grow their dividends.

He maintains a well-diversified portfolio, with some 66% invested in blue-chip UK-listed companies. These tend to be international companies invested in economies likely to grow faster than the UK.

The best overall performance among the UK trusts was delivered by . Its annual dividend payout rose by 4.5% last year. Its yield remains relatively low, but that is partly due to its strong share price performance.

Managers Francis Brooke and Hugo Ure are known for their cautious investment approach and a focus on capital protection. So its portfolio tends to be biased towards defensive sectors, such as consumer goods companies with strong brands. Last year the managers reduced the trust's exposure to utilities and increased its holdings of financial stocks instead.

Another strong performer was , which announced a 4.2% increase in its dividend last year. In addition, it paid a special dividend in June, passing on the special dividends it had received from companies it invests in.

Manager Mark Barnett favours companies which offer visibility of revenues, profits and cashflows. Key contributors to the trust's performance last year were its holdings in tobacco companies and some of its investments in the financial services sector. Its lack of exposure to banks and mining companies also helped.

Although continued to deliver on the income front last year, its capital performance has failed to improve. We have therefore decided to switch out of this holding into instead; see "The Switches" section below for our rationale.

Global diversification

For income investors, it makes sense to cast the net as widely as possible to gain access to different sources of income around the world. Internationally oriented trusts can invest in a wider range of companies and provide access to industries not represented in the UK.

When the portfolio was set up, we therefore opted to place 60% in trusts investing outside the UK, although some of the global trusts such as and also have significant UK holdings.

The largest holding is . The reasons for making it our largest holding is our belief in the skills of the manager, Bruce Stout. At the time, we felt the trust's high exposure to Asia and the emerging markets would help its long-term performance. Over the past few years, however, this exposure has led to a fall in its share price.

However, we still believe Murray International will perform well in the long run given its emphasis on companies with sound business models, strong market positions and competent management focused on shareholder interests.

Best for capital

The best capital performance, and best total return across all our holdings, was produced by Majedie Investments. However, it produced the least income. Nevertheless, part of its objective is to increase its dividends by more than inflation over the long term, so we think it is a useful holding.

It holds shares in Majedie Asset Management, which runs open-ended investment funds, and it also invests in Majedie funds such as , currently one of the top-performing income funds.

Scottish American is another of our internationally diversified holdings. By 2015 it had racked up 35 consecutive years of dividend increases. It invests mainly in global equities, but can also hold other asset classes and currently has 13% invested in commercial property and 4% in bonds.

Such has been the popularity of the trust that it has been trading at a premium to net asset value (NAV) recently. We have therefore scaled back the suggested stake in this trust for new investors.

A further 25% of our original trust portfolio was invested in more specialist trusts - , and . Although all three have more or less delivered as expected on the income front, their capital performances have been more varied.

Both the JPMorgan and the Middlefield trusts lost considerable ground and their share prices fell from premiums to discounts to NAV. As a result, and in order to focus on stronger markets, we have therefore decided to switch out of the JPMorgan trust into (see the box above).

Relative to their size, our two smallest holdings have produced the highest levels of income. However, measured by total return, Middlefield Canadian Income has had a poor year due to concerns about Canada's commodity-oriented economy and the strength of the pound versus the Canadian dollar.

But the trust's exposure to resources-related stocks has been reduced significantly and its largest exposure now is to the financial sector, in which the managers expect to benefit from rising interest rates. We have decided to retain this holding for the time being.

Princess Private Equity, by contrast, has had a very good year on the capital growth front and its share price discount to NAV has narrowed significantly. Its yield remains high, although, as Numis Securities points out, it is essentially distributing from capital using the profits from disposals, and is not aiming to cover the dividend from net revenue from its portfolio.

This approach is unlikely to cause a problem according to Numis; it is positive on the outlook for the trust's NAV growth, and believes its dividend is sustainable given the strength of its balance sheet and the diversified nature of its portfolio.

The switches

Out - Temple Bar

Temple Bar has attractive features. It has been increasing its dividends for more than 30 years and it has low ongoing charges of 0.48%. However, the contrarian approach taken by its manager, Alastair Mundy, which involves investing in unloved, mainly larger companies that he expects to recover, has held back its capital performance in recent years.

While we believe that this trust will continue to deliver an increasing income and Mundy's approach could pay off for patient investors over the longer term, we think that our alternative choice offers better prospects for the foreseeable future.

In - Diverse Income

This trust is relatively new, having been launched by the in 2011. However, its managers, Gervais Williams and Martin Turner, are very experienced and it has already acquired a good performance record. Williams, who is managing director at Miton, was a well-known manager of smaller companies funds at (now defunct) Gartmore, while Turner is also a small and medium-sized companies specialist.

Although Diverse Income can invest in companies of any size, it has a bias towards medium and smaller companies, including those listed on AIM. It has already built up revenue reserves of 0.37 years' dividend. Its aim is to progressively increase its dividend.

Out - JPMorgan Global Emerging Markets Income

Although JPMorgan Global Emerging Markets Income has delivered on the income side, its capital performance has suffered over the past year as emerging markets generally have fallen from favour. Although we would expect this trust to come good in the long term, it is difficult to see a rapid recovery in emerging markets anytime soon so, given our exposure to emerging markets via other holdings, we have decided to cut losses.

In - Schroder Oriental Income

Although this trust has lost ground recently, it has achieved a good longer-term performance record under the management of its highly experienced investment manager Matthew Dobbs. The Asian economies are mainly net importers of commodities for their manufacturing industries, so they are benefiting from lower prices.

Dobbs has pointed out recently that there is still a wide and growing choice of Asian companies paying above-average dividends, with good prospects for dividend growth despite recent problems. His focus on well-financed companies should ensure the trust's performance recovers rapidly as sentiment towards the region improves.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.