Huge changes to UK bank sector forecasts

20th July 2016 11:39

by Lee Wild from interactive investor

Share on

The FTSE 350 Bank index is up 14% since the Monday after Brexit. It's only down 5% since the post-referendum crash, prior to which it stood at highs not seen since mid-January. But the stats don't tell the whole story and, ahead of second-quarter results season which kicks off next week, UBS has decided it's time to reflect the new set of circumstances in its own numbers.

"The UK's EU referendum outcome shifted our domestic macro outlook from decent expansion to juddering halt," explains UBS analyst Jason Napier. "We now expect two rate cuts in second-half 2016, the resumption of quantitative easing and a worse-than-halving of the ten year gilt yield."

Unemployment is also tipped to rise from 5% to 5.8% and inflation will surge to 3.4% next year. Investment spend is also vulnerable despite the weak pound making our exports more competitive, as is residential and commercial property to which banks are significantly geared.

It's why estimates now factor in lower margins, driven largely by lower interest rates and more cautious lending, lower loan growth and higher bad debts. Given their business mix, and escape the worst of the downgrades.

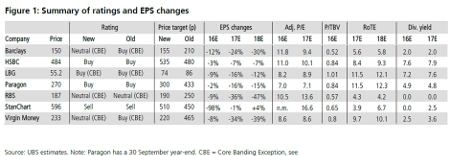

Earnings per share estimates for HSBC drop by a modest 7% for both 2017 and 2018, while forecasts for Standard Chartered dip by just 1% for next year and rise by 4% in 2018.

, and take a pasting given "depressed profitability and dependence on volume growth to drive positive operational gearing". UBS takes around a quarter off profit estimates for the next few years, but forecasts for the other two are cut by between 34% and 47%.

Of course, there's plenty of speculation over dividends. "Capital levels look sufficient to deliver forecast dividends but the trajectory for capital build is now substantially weaker," writes Napier.

has only just started paying out to shareholders after a post-financial crisis break, but even though UBS thinks it may use Brexit as a valid excuse to moderate distributions, it's still the broker's top pick of the large-cap banks and offers a prospective yield of over 7%.

HSBC is "arguably is over-distributing", reckons Napier, although it yields 7.9% based on estimates for 2017.

"Catalyst-wise the UK banks are in a tough spot," admits Napier. "second-quarter 2016 results won't be particularly relevant and the depth of the domestic slowdown remains to be seen. Still, we think the Lloyds and share prices have over-reacted: we keep these as 'buys' and our top picks."

UBS's price target for Lloyds falls from 86p to 74p, still implying 34% upside and, while the target for Paragon is slashed by almost a third, there is still potential upside of 11% to the new 300p target.

However, UBS downgrades Barclays to 'neutral' from 'buy' based on a weaker outlook for domestic and capital market banking, compounded by increased regulatory uncertainty. Lower growth and margins force an identical move on Virgin.

Elsewhere, HSBC remains a 'buy' and Standard Chartered a 'sell' with targets at both up substantially to 535p and 510p respectively, as the weak pound offsets lower earnings per share estimates.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.