Why mining bears are worried

21st September 2016 12:35

by Lee Wild from interactive investor

Share on

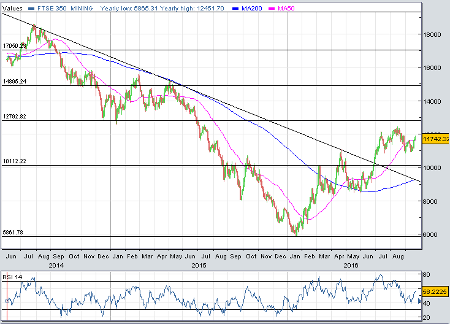

Investors in mining shares have enjoyed an unbelievable 2016 so far. The FTSE 350 Mining index is currently up 61%. It's more than doubled from its January low. But one team of City analysts has just upgraded the sector and profit forecasts by as much as 98%! Expect a return to the dividend list sooner than expected.

With the fourth-quarter almost upon us, and after some decent results in August, sector outperformance has dried up as steel and iron ore prices have fallen back. That may be a relief to Barclays' clients, who have been underweight the sector and remain cautious.

However, a 67-page research note produced by Barclays Wednesday may force them to reconsider.

"The uncertainty over the direction of the [US dollar], some recent positive economic data (and statements) from China plus the faint whiff of infrastructure-based fiscal stimulus in the West are challenging this position," writes the broker.

And the mining sector is cheap, too. It reminds Barclays of the pre-supercycle era "where a cynical market would discount spot commodity prices and then apply a market average earnings multiple".

Based on spot commodity prices, diversified miners - , , , , , and - trade on just 9.5 times earnings per share (EPS) estimates for 2017. That compares with a broader market "bereft of earnings growth and trading on multiples twice these levels".

"Add to that cautious sector positioning and also the potential for dividend reintroduction and it is no wonder the bears are worried. We move our European mining industry view to 'positive' as we enter Q4, which, if prices hold, could deliver a 20%-plus performance."

Iron ore prices

Hiking assumptions for iron ore prices in 2017 from $45 per tonne (/t) to $50/t helps trigger a sharp increase in average EPS forecasts - 78% for 2016, 92% for next year and 98% in 2018. It is, however, worth remembering that these "extremely material" changes to profit forecasts reflect the sensitivity typical when you're coming from a very low base.

Barclays doesn't expect some spot prices to last either, particularly coking coal. However, every day it stays around current levels, debt keeps falling. To illustrate, the broker expects degearing of 31% between 2015 and 2018 on its own commodity price forecasts, but on current prices it would improve to 44%. That's great news for income investors.

"Management and boards, in our view, are fearful of spending on M&A," says Barclays, "and only the best projects will receive funding, which leaves the re-introduction of dividends earlier than expected as an increasingly likely and powerful catalyst (as opposed to the oil sector)."

After running the numbers again, Barclays upgrades Anglo American to 'equal-weight' based on valuations, short-term cashflow and a better performance in diamonds, with the price target increased by 54% to 845p.

Rio Tinto is still rated 'overweight' with 2,800p target and BHP Billiton 'equal-weight' and 990p. S32 is upgraded to 'overweight' with 160p target.

On the downside, take a break from Hochschild Mining, suggests Barclays, cutting its rating after a strong run to 'equal-weight' with 280p target. Gem Diamonds drops from 'overweight' to 'underweight' and the price target is slashed from 180p to 110p.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.