Tactical Asset Allocator: Build up cash and wait for markets to fall

24th May 2017 08:56

by Ceri Jones from interactive investor

Share on

The principal driving forces in many markets currently are political factors, among them president Donald Trump's failure to deliver on his promises in the US and the UK government's struggle to extract the UK from the EU. There is no shortage of international risk either, notably in the unnerving shape of North Korea.

But first to France, where Emmanuel Macron must now attempt to fix the sluggish French economy and boost employment, as the alarming prospect of a Front National government led by Marine le Pen disappears for now.

Le Pen's fate was more or less sealed in an acrimonious pre-election debate watched by 16.5 million people. Since then, the German DAX and French CAC indices have both risen, confounding expectations that 2017 would be a difficult year for European markets.

Macron wants closer cooperation within the EU. However, he is a political novice, and his strategy to tighten labour regulation could hit the buffers.

Uncertainty in the US

In the US, while Trump's long-term credibility regarding his election promises on tax cuts and healthcare provision is fragile, the labour market is enjoying a spurt of recovery. Non-farm payrolls increased by 211,000 in April - better than average for the month and very welcome following March's disappointing data.

The strong employment figures have been deemed sufficient to keep the US Federal Reserve on a path of interest rate rises, even though US inflation has been falling. But that downward trend, together with the weak oil price, should alleviate pressure on the Fed to implement a string of rate hikes in quick succession.

Higher US rates was one reason why demand for gold fell by 18% in the first quarter of the year compared with the same quarter of the previous year. Then in early May the price of gold suffered its largest weekly fall of the year so far, as the backlash from jobs data kicked in.

Complex global picture

In contrast, demand in China for gold soared by 30% in the first quarter, in spite of the strength of China's economic recovery over the past year - which, at 6.9% GDP growth year-on-year, far exceeded consensus expectations. Industrial production and retail sales are now progressing steadily, but investors are worried about China's overheated property market, North Korean belligerence and potential currency weakness as the Chinese authorities change tack.

Central bank hawkishness is needed to maintain financial stability and reduce excessive debt in parts of the corporate sector (which the People's Bank of China can achieve by raising interbank lending rates) - tasks made all the more pressing politically by long-awaited Communist Party of China leadership changes planned for the autumn.

In the UK the index has underperformed, thanks to a strong pound and falling oil prices - Brent tumbling to its lowest level since last November. Much depends on whether Opec decides to make severe production cuts, as it must if it is to stabilise prices at a time when Trump is encouraging greater oil production in the US.

Strong purchasing managers index (PMI) figures have supported the pound, the strength of which is a positive sign for the UK economy but has dragged down large exporting stocks.

However, higher interest rates and the UK's momentous decision to leave the EU have hurt property funds, as international investors look to invest elsewhere in Europe - affecting our holding, for example.

Although the overall economic picture is quite benign, no sectors or regions are compelling over the short term. It makes sense to keep money on the sidelines and wait for a selloff, as valuations are very high. The proverb 'sell in May and go away' is a mile off the mark, however. Historically, May has produced positive returns more often than not.

June would be a better month for investors to reduce their equity holdings - but it doesn't rhyme with St Ledger's Day, the second Wednesday in September, when investors are exhorted to return to stock markets. September is actually the month that requires the most concentration: historically, it is the worst month of the year for investments.

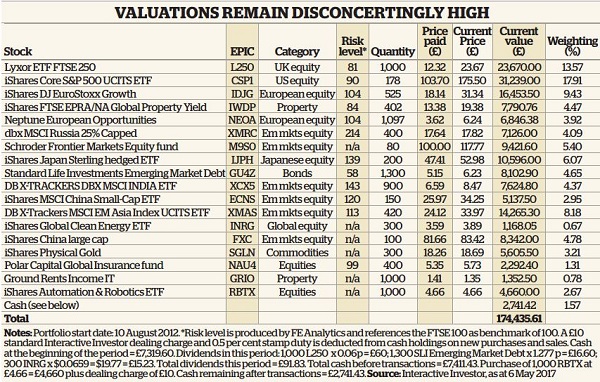

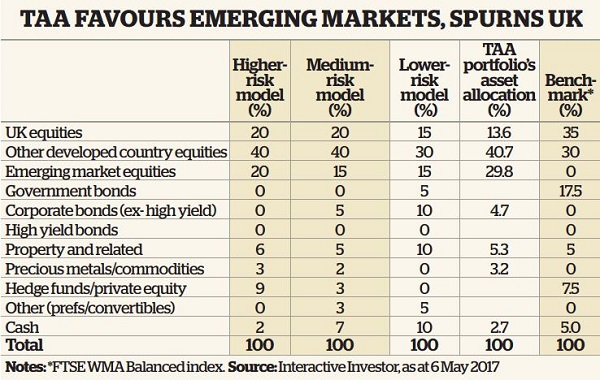

Longer term, the big themes such as ageing demographics and a new technological revolution remain compelling. These can be accessed through BlackRock ETFs: the , , the and the . We will invest some of our cash in RBTX on the grounds that its US tech stock bias should provide diversifi cation against other large-cap holdings. Its biggest holdings include Largan Precision, Advantest Corp and Topcon, and only one holding, , is bigger than 1.9%.

One interesting shorter-term opportunity is a global preferred securities Ucits fund from US asset manager Cohen & Steers. This aims to generate high income and capital appreciation by investing in a portfolio of global preferred securities. These pay income but are actually a form of equity that lies between common stock and senior debt in a company's capital structure.

So, in the event of a company failure, preferred securities holders are paid dividends before holders of the common stock. Cohen & Steers' US-based Preferred Securities and Income fund is the largest such fund in the world.

Some ETFs invest in preferred securities - the iShares International Preferred Stock (IPFF) and the SPDR Wells Fargo Preferred Stock ETF (PSK), for example. But they are listed in the US and primarily track US instruments.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.