Where to find 'cheap' US stocks

1st February 2018 09:29

by Ceri Jones from interactive investor

Share on

The market, it seems, is simply not interested in the lack of credibility around the Trump administration, which has been given vent in Michael Wolff's book, Fire and Fury: Inside the Trump White House; nor is it concerned by the continuing antagonism between the US and North Korea. The rally shows no sign of waning, despite high valuations and an eery lack of volatility.

There is growing divergence amongst commentators about what we can expect next. While it seems sensible to take the view that US equity indices - which are at all-time highs, boosted by positive sentiment and a soaraway information technology sector - are in melt-up phase, a growing coterie of analysts seem to believe that the Dow Jones could hit 50,000 by 2024 - nearly double its current 25,295.

They argue that the new tax reform bill will result in a massive boom for corporate America, while at the same time there could be a game-changing shift out of bonds and into equities by institutional investors with trillions of dollars at their disposal.

Self-evidently, higher earnings assisted by lower tax rates should make valuations appear more attractive, given that earnings are the denominator of one of the more common measures of valuation in the market - the price/earnings ratio (PE).

Tax cuts to lift earnings

And there is also a good case that the new tax system, which allows 100% write-off of capital expenditure on short-lived assets in the year they are made, will help companies that decide to renovate their premises or build new factories, spurring growth at companies such as DIY firm .

For most private investors, however, at this stage of the cycle it is possibly better to pick off sectors that have not enjoyed the full exhilaration of the nine-year bull run.

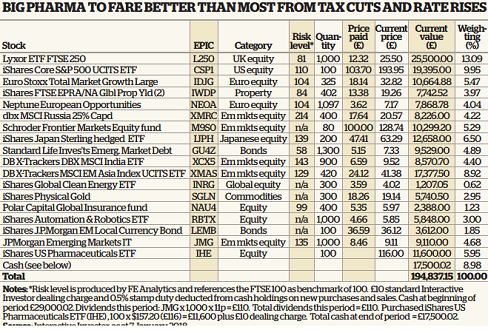

For example, the US healthcare sector is still trading on some of its lowest valuations since the financial crisis owing to uncertainty over healthcare regulation - in particular Trump's attempts to repeal Obamacare and overhaul pharmaceutical drug pricing policy.

Add in the benefits to the sector of Trump's repatriation policy, which plans to levy a 15.5% tax on repatriated cash earnings, compared with the previous 35% tax rate - and the sector could crawl out of the doldrums.

A recent Credit Suisse report found that US pharma makes up one third of the top 30 US companies with the most offshore cash. , for example, has $32 billion (£23 billion) of its total $41 billion in cash parked outside of the US.

The portfolio is going to stick its neck out by purchasing a holding in , unfortunately only listed on the NYSE Arca exchange.

The decision is also driven by the forthcoming US rate rises. The Fed is suggesting three in 2018, and they will encourage large institutional investors to sell up and shift into stocks which, owing to their scale, will have to be large caps such as pharma.

Furthermore, the bull market has been driven by quantitative easing and stimulus measures that tend to favour growth stocks, but there could be a return of the pendulum to value-oriented stocks with high relative dividend yields, low price-to-book ratios and/or low price-to-earnings ratios, particularly if uncertainty persists going forwards.

A more cautious strategy is to load up on European equities, which look relatively robust and have been under-bought compared with the UK and US. More European companies have beaten their earnings per share (EPS) than have missed them.

If the euro should drop lower, reversing last year's trend, then these businesses will have every reason to feel more confident about their sales abroad.

The geopolitical backdrop is now calm, and again there are undervalued sectors to pick off, such as European energy, financial companies and telecoms.

For investors who believe that the monetary policy direction in the US is still unclear and are already invested to the hilt in the US, Europe - still at the beginning of its monetary tightening cycle - has obvious appeal.

The other pressing question is whether China will falter. The Hang Seng index, now a barometer of China as much as Hong Kong, was a star performer last year, crossing the 30000 mark for the first time since 2007.

There has been no hint of a repeat of last November's bond rout, which took 3% off the CSI 300 index in a day as yields on sovereign debt and top-rated local corporate notes climbed to a three-year high.

However, with more than $1 trillion of local bonds maturing in 2018/19, it will become increasingly expensive for Chinese companies to roll over financing, dragging down equity prices - particularly financial stocks which, along with technology and telecoms, are again the ones on which most optimism is pinned.

Elsewhere in Asia, Korea's Kospi index also enjoyed particularly strong earnings growth as global economic growth picked up and supported the country's export-dependent economy.

Among developing markets, the Vietnam Stock index increased 47% in 2017, and there is room for a technical uplift if it is reclassified from frontier market to emerging market status.

The government's privatisation programme should help contain Vietnam's rising national debt and attract foreign investment.

Commodities are perking up. Palladium and platinum may be worth a flutter. Both owe their place in the commodity pantheon to catalytic converters and have been oversold in line with the depression in car manufacturing, but that is picking up globally, driven largely by increasing car ownership in emerging markets.

Finally, we cannot pass up the opportunity to comment on the increasing use of artificial intelligence to identify stock opportunities. Many of these systems are very bullish on prospects this year, with startlingly positive forecasts, but their future prognostications are based on historical data that's often only a decade old. This is surely something to worry about when the last decade has been so atypical in many ways (such as low interest rates), and even excludes the financial crisis.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.